Why Impatient Traders Got Wrecked by Market Swings

Published: Jun 15, 2026

• Updated: Jul 23, 2026

In this article:

- Why market swings punish impatient traders

- What past market shocks teach us

- Why impatient traders struggle

- How automation changes the behavior loop

- What to keep in mind

- What dollar-cost averaging can and can't do

- Explore these on Stash

- Bottom line

- Ready to invest on a plan, not on emotion?

- Important disclosures

- Frequently asked questions

Impatient trading means buying and selling on short-term market moves instead of following a plan. Across decades of market history, reacting to every swing has tended to cost investors money. It feels smart in the moment: the screen turns red, a headline screams, and you feel like you have to act right now.

The most recent example came in early June 2026, when a two-month rally in chip stocks reversed in a single session. Wall Street's "fear gauge," the VIX, posted its biggest one-day jump since March, and traders set a record with 7.8 million S&P 500 options contracts in one day, according to CNBC. On days like that, people who trade on emotion get whipsawed, while people who already set a plan barely flinch.

Send this to anyone who checks their portfolio every time the market drops. The gap between getting hurt by a swing and sitting through it is rarely genius. It is structure. That is why impatient traders got wrecked by market swings, while automated, scheduled investing stayed steady.

Why market swings punish impatient traders

Volatility turns every price move into a decision. A trader who checks prices five times a day can feel pressure to react five times a day. An automated investor has fewer chances to panic, chase, or second-guess.

Morningstar's 2024 Mind the Gap report put a number on the cost of those reactions. Fund investors earned about 1.1 percentage points less per year than the funds they owned over the 10 years ended Dec. 31, 2023, according to Morningstar. One big reason was timing: people moved money in and out at the wrong moments.

Picture two people during a 10% drop and the rebound that follows. Devon panics. He sells near the bottom to stop the bleeding, then waits for things to feel safe and buys back after prices have already recovered. He locks in the loss and misses the bounce. Maya, 32, invests $50 every Friday no matter what. During the drop, her $50 buys more shares; on the rebound, those shares recover with the market. Maya did not dodge the dip, but she never turned a paper loss into a real one.

When the market drops 10% | Impatient trader | Steady investor on a schedule |

|---|---|---|

First reaction | Sells to stop the loss | Keeps the next scheduled buy |

Next move | Waits, then buys back higher | Buys more shares at lower prices |

Decisions made | Many, under stress | One, made while calm |

Result | Locks in the loss, misses the bounce | Stays invested through the recovery |

If you are newer to investing, this is the idea behind The Stash Way: invest regularly. You invest a set amount on a set schedule instead of trying to pick the perfect day.

What past market shocks teach us

Every market shock feels new in the moment. The pattern rarely is.

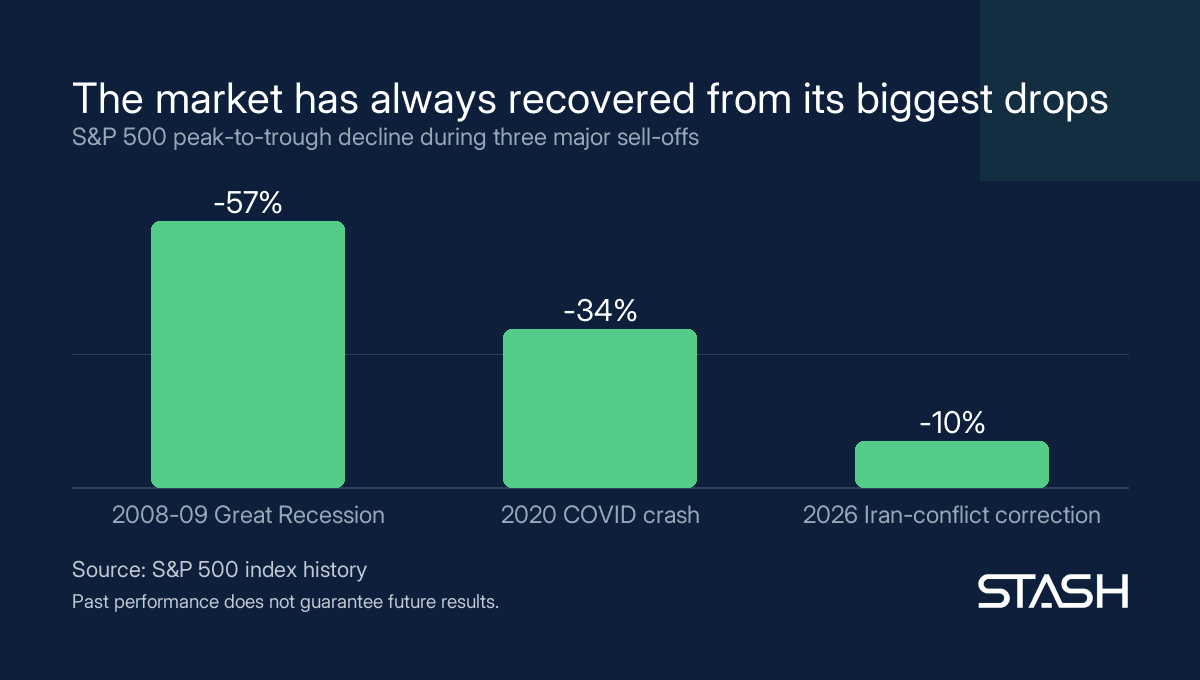

In 2008 and 2009, the financial crisis cut the S&P 500 roughly 57% from its October 2007 peak to its March 2009 low. Investors who panic-sold near the bottom turned a paper loss into a permanent one. Those who kept investing through the drop bought shares at lower prices and took part in the recovery that followed over the next several years.

The 2020 COVID crash was faster but rhymed. Stocks fell about a third in roughly a month, then climbed back to new highs within months. The people hurt most were the ones who sold at the bottom and waited too long to come back.

The most recent example is 2026. Renewed conflict involving Iran pushed oil prices above $110 a barrel and tipped major U.S. indexes into a correction. Headlines screamed, and impatient traders reshuffled their portfolios day by day. A steady investor on a schedule kept buying through it.

None of this means markets always recover on your timeline, and past recoveries do not guarantee future ones. The lesson is narrower: in a shock, the people who do worst are usually the ones who let the shock pick their trades.

Why impatient traders struggle

Impatient traders usually lose the battle against their own emotions before they lose to the market. Fast moves create a false sense of control. Selling can feel safe after prices fall. Buying can feel urgent after prices rise. Both reactions can turn a long-term plan into a string of short-term guesses.

The hard part is that market timing has to be right twice. You need to know when to get out. Then you need to know when to get back in. Miss either side and your result can change.

This is why day-trading culture can be rough for regular people with jobs, kids, rent, and a real life. You may not have hours to watch charts. You may be making choices while standing in line for coffee or sitting between meetings.

A steadier plan gives you fewer chances to make rushed moves. It also helps you focus on what you can control: your contribution amount, your account type, your time horizon, and your diversification. For a plain-English starting point, read how to start investing.

How automation changes the behavior loop

Automated investing puts your contributions on a schedule, so the decision happens once, when you are calm, instead of every time the news gets loud. That schedule helps separate your plan from your mood. It does not promise better returns and it does not protect against market loss. It gives your future self a rule to follow.

Think about your first 401(k) contribution. You likely did not choose each payday based on whether the market looked calm. Money came out on schedule. The same idea can apply to investing outside a workplace plan.

The value is behavioral. You decide on a repeatable amount when your head is clear, and the system carries out that decision later.

Stash is a regulated investment adviser, not a bank. The Stash plan includes financial guidance built into your phone. Other fees may apply; see the fee schedule for details. This is general guidance; what is right for you depends on your situation.

Ready to take the emotion out of investing? Set up recurring investments on Stash and let your plan run on a schedule, not on headlines.

What to keep in mind

Automation is useful, but it is not magic. Your investment mix still matters. Your emergency fund still matters. Your debt, income, and time horizon still matter. If your rent is due Friday, an automated investment on Thursday may not fit your cash flow. A steady plan should work with your real budget.

Here are a few questions to ask before you automate:

Can you cover bills before this transfer happens?

Do you have some cash set aside for surprise expenses?

Are you investing for a goal that is years away, not next month?

Is your money spread across different types of investments?

Do you understand that your balance can still go down?

Diversification matters most during choppy markets. It means you do not put all your money into one company, one sector, or one idea. The basics are in this complete guide to index funds.

What dollar-cost averaging can and can't do

Dollar-cost averaging means investing a fixed amount on a set schedule, like $50 every Friday, no matter the price. It can lower the pressure to time the market and smooth out your average purchase price over time. What it can't do: guarantee a profit, prevent losses, or protect you in a long downturn. It is a discipline, not a shield. The point is to keep one bad week from rewriting your whole plan.

Frequently asked questions

Why do impatient traders lose money in volatile markets?

Impatient traders often react after prices have already moved. They may sell after a drop or buy after a rally. That can turn normal volatility into repeated mistakes. Market timing also requires two hard calls: when to exit and when to re-enter.

Does automated investing prevent losses?

No. Automating contributions does not prevent losses, reduce market risk, or guarantee any result. Investments can rise or fall in value. A schedule can make your contributions more consistent, but your outcome still depends on markets, your portfolio, fees, taxes, and time horizon.

Is automated investing the same as dollar-cost averaging?

It can be. Dollar-cost averaging means investing a fixed amount on a regular schedule. Automating recurring contributions is one way to practice it. It can reduce the pressure to pick one perfect entry point, but it does not ensure a profit.

How much should I invest on a schedule?

There is no one number for everyone. A useful starting point is an amount that fits after bills, debt payments, and emergency savings. For one person that may be $10 a week. For another it may be more. This is general guidance, not personalized advice.

Explore these on Stash

These ETFs are available to invest in on Stash. This list is educational and is not a recommendation to buy any security.

iShares Core S&P 500 ETF (IVV) - Tracks the S&P 500

Schwab US Dividend Equity ETF (SCHD) - Focuses on dividend-paying companies

Bottom line

When markets swing, the edge is not predicting the next move. It is building a process you can live with, so a wild day in the market is not a wild day in your portfolio.

Ready to invest on a plan, not on emotion?

Stash helps everyday investors start with as little as $5 and build a long-term plan with guidance at every step.

Important disclosures

Investing involves risk, including possible loss of principal. This article is general education, not personalized investment, tax, or legal advice. Automating contributions can help you invest consistently, but it does not guarantee performance or protect against losses. Before investing, consider your budget, goals, time horizon, and risk tolerance.

Investing involves risk, including the possible loss of principal. See full disclosures at www.stash.com/disclosures.

Educational only and is not a recommendation to buy, sell, or hold any security. See full disclosures at www.stash.com/disclosures.

Stash is not a bank. Banking services are provided by a partner bank, and FDIC insurance is provided through that partner bank.

Educational only and does not constitute investment, legal, accounting, or tax advice. See full disclosures at www.stash.com/disclosures.

Written by

Team Stash

We want to turn money into a source of hope and opportunity. We teach people how to build good habits, save more and make it easy and affordable to get started investing. So far, we’ve helped over 6 million people create a more secure financial future with our expert advice and award winning investing app.

Related articles

guides

Jun 26, 2026

Money in 10: the numbers that prove boring investing wins

guides

Jun 15, 2026

Why Impatient Traders Got Wrecked by Market Swings

robo-advisor

Mar 19, 2026

FAQ: Stockpile

guides

Jan 23, 2026

Closing an IRA? State Withholding Requirements

guides

Jan 16, 2026

Age of majority

investing

Jan 13, 2026

FAQ: Personal Portfolio

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.