Aug 16, 2023

Financial Literacy: The 7 Principles of Managing Your Money

Have you ever wondered how to make the most of your hard-earned cash? Have you ever felt overwhelmed by financial terms or uncertain about where to invest your money? If so, you’re certainly not alone. Managing money doesn’t come naturally to most people, and it’s no surprise why. Personal finance is rarely taught in school, yet it’s a skill everyone needs to thrive in life. Enter financial literacy: a spectrum of knowledge and skills that enable you to navigate the complex world of personal finance, plan for your future, and achieve your financial goals.

Whether you’re a young adult entering the workforce, a recent graduate juggling student loans, or just someone trying to be smarter with your money at any point in your life, understanding financial literacy can change how you handle your finances for the better.

This guide will introduce you to the seven core principles of managing your money: earning, budgeting, saving and investing, debt management, understanding credit, safeguarding your financial well-being, and financial planning. By the end, you’ll have actionable tips to feel more in control of your finances and take confident steps toward financial stability.

What is financial literacy? Financial literacy goes beyond just managing money; it encompasses a spectrum of knowledge and skills that enable you to navigate the complex world of personal finance, plan for your future, and achieve your financial goals. |

|---|

Why is Financial Literacy Important?

Simply put, financial literacy means having the knowledge you need to manage your money in a way that supports your lifestyle and goals—and, importantly, the ability to apply that knowledge in your everyday life.

At its core, financial literacy is about empowerment. It helps you make informed choices, avoid common money mistakes, and build a secure financial future. Mastering these basics can prevent stress, save time, and provide long-term financial security.

Think about it—your finances touch every aspect of your life. Rent payments. Grocery bills. Retirement savings. Emergencies. By improving your financial knowledge, you’ll not only eliminate guesswork, but also take charge of your future.

The 7 principles of financial literacy

Financial literacy empowers you to make informed decisions about your money, helping you build a secure future and achieve your financial goals. This article will explore the five basic principles of financial literacy: earn, save & invest, protect, spend, and borrow, providing you with actionable insights to enhance your financial knowledge and make the most of your resources.

Earn

Budgeting

Save & invest

Debt management

Credit

Borrow

Protection

Financial planning

overwhelmed by financial terms or uncertain about where to invest your money? If so, you’re certainly not alone. Managing money doesn’t come naturally to most people, and it’s no surprise why. Personal finance is rarely taught in school, yet it’s a skill everyone needs to thrive in life. Enter financial literacy: a spectrum of knowledge and skills that enable you to navigate the complex world of personal finance, plan for your future, and achieve your financial goals.

Whether you’re a young adult entering the workforce, a recent graduate juggling student loans, or just someone trying to be smarter with your money at any point in your life, understanding financial literacy can change how you handle your finances for the better.

This guide will introduce you to the seven core principles of managing your money: earning, budgeting, saving and investing, debt management, understanding credit, safeguarding your financial well-being, and financial planning. By the end, you’ll have actionable tips to feel more in control of your finances and take confident steps toward financial stability.

Principle 1. Earning: Empowering your potential

In order to manage your money, you have to first have money to manage. Whether you make your income from a full-time job, part-time work, freelancing, or running a small business, financial literacy can help you take more control of how much money you have coming in. It also equips you to increase your income over time to meet your long-term goals.

When it comes to earning, financial literacy is about developing skills, pursuing education, and securing employment that enables you to earn the income you need now and in the future. Increasing your earning potential opens doors to financial stability and growth. Your income is the foundation upon which your financial stability rests.

Tips to empower your earning potential:

Diversify your skills: In today’s ever-changing job market, diverse skill sets are invaluable. Invest in learning new skills or expanding your expertise. The more versatile you are, the more opportunities you’ll have to earn.

Negotiate your worth: Don’t shy away from negotiating your salary with your employer. Research market standards and present your achievements confidently. Negotiating effectively can significantly boost your income over time.

Side hustles: With the continual development of new technologies, the possibilities for side hustles are endless. Whether it’s freelance work, gig jobs, online tutoring, or starting a small business, a side hustle can supplement your income and accelerate your financial progress.

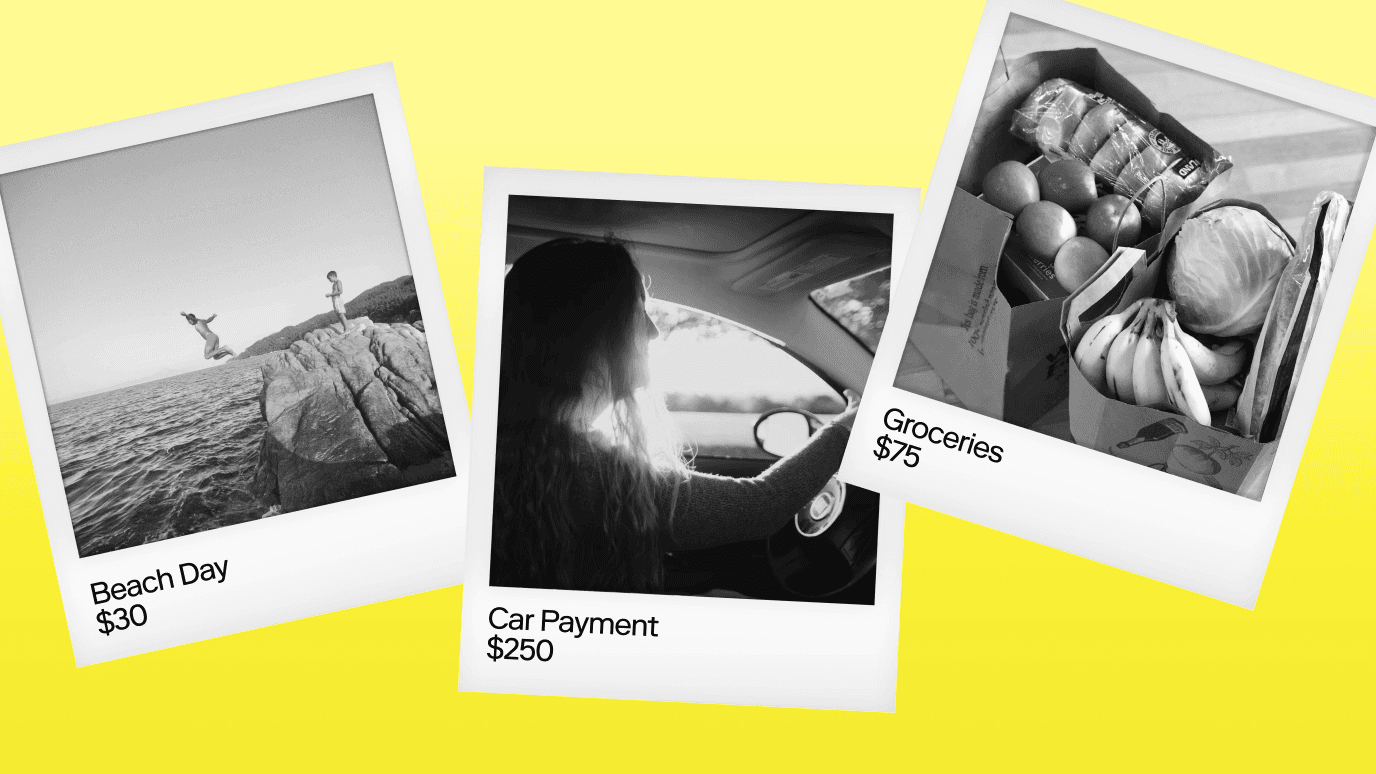

Principle 2. Budgeting: The foundation of money management

Budgeting is the backbone of putting financial literacy into action. With an effective budget in place, you can understand where your money goes and ensure you’re living within your means—as well as put money away for the future. A solid budget helps you divide your income among essentials, discretionary spending, and savings or investing for the future. By making a budget and sticking to it, you can ensure you’re not overspending and feel more empowered to make informed choices about where your money goes.

Tips for effective budgeting:

Track your income and expenses: Start by writing down all your sources of income and every expense, from rent to your morning coffee. Budgeting apps can make this process simpler.

Use a budgeting strategy: Deciding how to allocate your income can be a bit overwhelming. A budgeting strategy gives you a clear framework to build a budget that makes sense for your lifestyle.

Review it regularly: As your life evolves, so will your budget. Regularly review and adjust your budget approach to align with changes in your income, expenses, and priorities.

Principle 3. Saving and investing: Building a bright financial future

Financial literacy gives you tools to set yourself up for future financial success. Saving and investing are the cornerstone of reaching your financial goals. Every dollar saved or invested today sets you up for more financial freedom tomorrow.

The power of saving

Saving money helps you work toward your bigger aspirations—like taking a dream vacation, buying a new car, or putting a down payment on a house. It also provides a financial safety net to cover emergencies and help you break the cycle of living paycheck to paycheck. A well-structured savings plan involves setting aside a portion of your income regularly, working toward both short-term and long-term objectives. Even if you can’t save much each month, you can still start a savings habit, and the sooner you get started, the more time you have to increase your nest egg.

Tips for smart saving:

Take advantage of compound interest: Imagine a snowball rolling down a hill, growing larger and faster as it goes. Compound interest works similarly—your money grows over time, earning interest not only on your initial deposit but also on the interest earned. Look for savings accounts with high interest rates, and keep your money in the account as long as possible to take advantage of compounding.

Build an emergency fund: Emergencies happen, whether it’s a car repair, medical bill, or unexpected job loss. Aim to build an emergency fund that covers approximately three to six months’ worth of living expenses. By putting aside a bit of money each month, you can avoid pinching your budget or going into debt when life throws you a curveball.

Choose accounts with the best rates: Earning interest is one smart way to make your money work for you. The higher your interest rate, the more your money can grow and benefit from compound interest. Look for options like high-yield savings accounts or certificates of deposit (CDs) that offer better rates than traditional savings accounts.

The power of investing

Saving is ideal for building an emergency fund and reaching short-term goals, but investing can help you build wealth into the future. Over the long term, returns from investments often outperform savings account interest rates and outpace inflation—which is helpful when you’re looking at financial goals that are decades ahead. Even if you’re brand-new to investing, you can get started, and the sooner you start, the more time you have to work toward your future.

Tips for investing as a beginner:

Educate yourself: Learn about different investment options, such as stocks, bonds, mutual funds, and real estate. Familiarize yourself with how the stock market works. Understand how diversifying your portfolio can minimize risk and maximize potential returns. It likely won’t take long for you to grasp the foundations of investing.

Assess your risk tolerance: All investing comes with some level of risk. That’s why it’s important to understand your personal risk tolerance, which is the level of uncertainty you’re comfortable with in your investment portfolio. This can guide your investment strategy and help you make choices that support your goals.

Consider a robo-advisor: If you’re uncertain about how to start investing, you might want to look for a brokerage with a robo-advisor. These tools can automatically build and manage a portfolio for you based on your preferences, goals, and risk tolerance. As an added bonus, they’re generally less expensive than using a personal financial advisor.

Invest for retirement: It’s never too early (or too late!) to start planning for retirement. Start by calculating how much you need to retire based on your current age and desired retirement age. Then explore your options for tax-advantaged retirement accounts, such as a 401(k) from your employer or an IRA.

Principle 4. Debt management: Avoiding the pitfalls of debt

Most people find themselves in debt at some point. Sometimes it’s essential for investing in yourself, like getting a college degree or buying a house. Other times, debt comes along because of unexpected events—like medical bills or a big car repair—or relying on credit cards or personal loans for living expenses. What’s important to remember is that not all debt is inherently bad, but too much of it (or the wrong kind) can trap you in a cycle of strained finances. The trick is managing debt so that it supports your financial health.

It may help to think of debt as being either “good debt” or “bad debt.” Student loans or mortgages, for example, can be considered “good debt” when managed responsibly, because they can increase your earning potential or net worth. On the other hand, things like credit cards and personal loans are often considered “bad debt,” because high interest rates can quickly cause your debt to spiral out of control.

Whether it’s the “good” or “bad” type, carrying high debt over time can have a negative effect on your life, from restricting your cash flow and ability to save money to impacting your credit score. It can also cause a significant amount of stress. Paying off debt can free up your money for saving, investing, or simply enjoying life with less financial worry.

Tips for managing debt:

Know what you owe: List all your debts, including amounts, interest rates, and minimum payments. Calculate how much you spend on debt payments each month so you know how much of your income is devoted to paying off loans and credit cards.

Pay off high-interest debt as soon as possible: Carrying debts with high interest rates can significantly impact your ability to save money for the future—and can even make it hard to cover essential expenses. Use the avalanche method (paying off high-interest loans first) or the snowball method (paying off smaller debts first to build momentum) to reduce those debts.

Avoid new debt: Only borrow money when absolutely necessary, borrow within your means, and always plan how you’ll repay it. Keeping enough in your emergency fund can help you avoid going into more debt when you have to deal with a large, unexpected expense.

Principle 5. Understanding credit: Building and maintaining a good credit score

Your credit score impacts everything from renting an apartment to getting a car loan or credit card. Some employers even consider your credit score when making hiring decisions!

Your credit score is a three-digit number that represents your creditworthiness. Ranging from 300 to 850, the higher your score, the better your credit. A higher score means you’re considered trustworthy by lenders. That makes it more likely for you to be approved for things like a mortgage or car loan and qualifies you for lower interest rates.

Building good credit early can open doors to financial opportunities as your needs evolve. And as an added bonus, paying your credit card balance in full each month will help you avoid accumulating interest charges.

Tips for building a strong credit score:

Pay bills on time: Your payment history makes up 35% of your credit score. Set reminders or use autopay to avoid late payments on bills, including things like rent/mortgage payments, utilities, your phone plan, and existing debts.

Keep credit utilization low: Aim to use less than 30% of your available credit. For example, if you have a credit card with a $6,000 limit, try not to charge more than $2,000 on it before paying off the balance.

Don’t close old accounts: Your credit history length matters, so keep older accounts open, even if you’re not using them. The only exception is accounts that have fees; closing those saves you from paying unnecessary costs if you don’t need them.

Check your credit report: Regularly review your credit reports from major credit bureaus including Experian, TransUnion, and Equifax to ensure accuracy and spot any fraudulent activity. You’re entitled to one free copy of your credit report from each agency every year.

Principle 6. Protection: Safeguarding your financial well-being

Life is full of uncertainties, and that includes your financial picture. A key aspect of financial literacy is thinking through potential dangers to your monetary well-being and taking protective measures. As the old saying goes, an ounce of prevention is worth a pound of cure. Even if some concerns seem unlikely or far in the future, take time to consider different scenarios and how you can safeguard yourself and your finances.

Tips for safeguarding your finances:

Insurance coverage: Insurance is there to cover you when an unexpected event causes you financial hardship. If you own a car, you’re required to carry car insurance in case of an accident. But there are other scenarios that can disrupt your finances, like an injury that prevents you from working. Look into things like disability insurance (which helps if you’re physically unable to work for a short or long time), life insurance (which can provide for your family if you pass away), and different health insurance options to cover your medical needs.

Estate planning: What will happen to your money after your death? Regardless of your age, it can be wise to plan ahead for the eventuality. Having a will and an estate plan ensures your assets are distributed according to your wishes and minimizes potential conflicts. Estate planning gives you peace of mind now and can help your loved ones more easily deal with the financial repercussions later.

Identity theft prevention: If your identity is stolen, it can open you up to financial liability. Scammers can rack up fraudulent credit card charges, drain your bank account, open new accounts in your name, and more. You could wind up with a damaged credit score and find yourself out a lot of money. Safeguard your personal and financial information by using strong passwords, regularly monitoring your accounts, and being cautious about sharing sensitive data online.

Principle 7. Financial planning: Setting and achieving long-term goals

As you build your financial literacy, you’re likely to recognize that truly understanding money management calls for a future-focused perspective. Without a plan, it’s easy for money to slip through the cracks. Financial planning gives you a roadmap to achieve goals like buying a house, traveling the world, or retiring comfortably.

Keep in mind that a good financial plan isn’t rigid—it’s flexible and adapts as your life changes. The idea is to lay out a strategy that can carry you far into the future, then periodically revisit your roadmap and adjust it as your circumstances change. You might not know exactly where you’ll be 10 or 20 years from now, but you can envision what you want to achieve, make a plan to get there, and continually adjust as needed.

Tips for making a financial plan:

Set SMART goals: Your goals should be specific, measurable, achievable, relevant, and time-bound (aka, SMART). For example, having a general goal of “save for a vacation” isn’t very useful for taking action. Instead, you could set a SMART goal such as “I will save $3,000 for a vacation in 12 months. I will put $250 in a savings account every month.”

Break goals into milestones: It can be overwhelming to save for something big. Make it more achievable by breaking goals down into smaller milestones. For instance, if you have multiple credit cards to pay off, it can be less overwhelming to focus on paying off one balance at a time. Or if you're saving for something really big over many years, break that down into how much you can save each month.

Work with a professional: If your financial situation feels overwhelming, a financial planner can offer personalized advice. Financial planners can help with all aspects of your money management, from getting out of debt to saving for retirement to estate planning and more.

Build your financial literacy and take control of your future

Financial literacy isn’t something you master overnight—it’s a lifelong skill that grows with practice. Start by focusing on the seven principles above to begin building a solid financial foundation. Over time, you’ll master more and more skills to support financial stability.

Ultimately, a strong sense of financial literacy can help you make informed decisions that align with your long-term goals. And in addition to the practical benefits, financial literacy can give you a sense of control that makes managing your money feel less stressful and more empowering.

SMART goals

Use the SMART framework to refine your goals:

Specific: Clearly define what you want to achieve.

Measurable: Set concrete criteria to track your progress.

Achievable: Ensure your goals are realistic and attainable.

Relevant: Align your goals with your values and priorities.

Time-bound: Establish a deadline for achieving each goal.

Investing made easy.

Start today with any dollar amount.

Written by

Team Stash

We want to turn money into a source of hope and opportunity. We teach people how to build good habits, save more and make it easy and affordable to get started investing. So far, we’ve helped over 6 million people create a more secure financial future with our expert advice and award winning investing app.

Related articles

budgeting

May 04, 2025

How to Build Credit from Scratch in 2025

budgeting

Apr 27, 2025

Who gets the insurance check when a car is totaled?

budgeting

Apr 09, 2025

How to Make Extra Income While Working Full-Time

budgeting

Apr 08, 2025

How Much Does the Average American Make?

budgeting

Apr 07, 2025

How to Calculate Monthly Income

budgeting

Mar 14, 2025

How to Budget for Large Expenses

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.