Short-term vs. long-term investing: a simplified guide

Published: May 02, 2024

• Updated: Jun 09, 2026

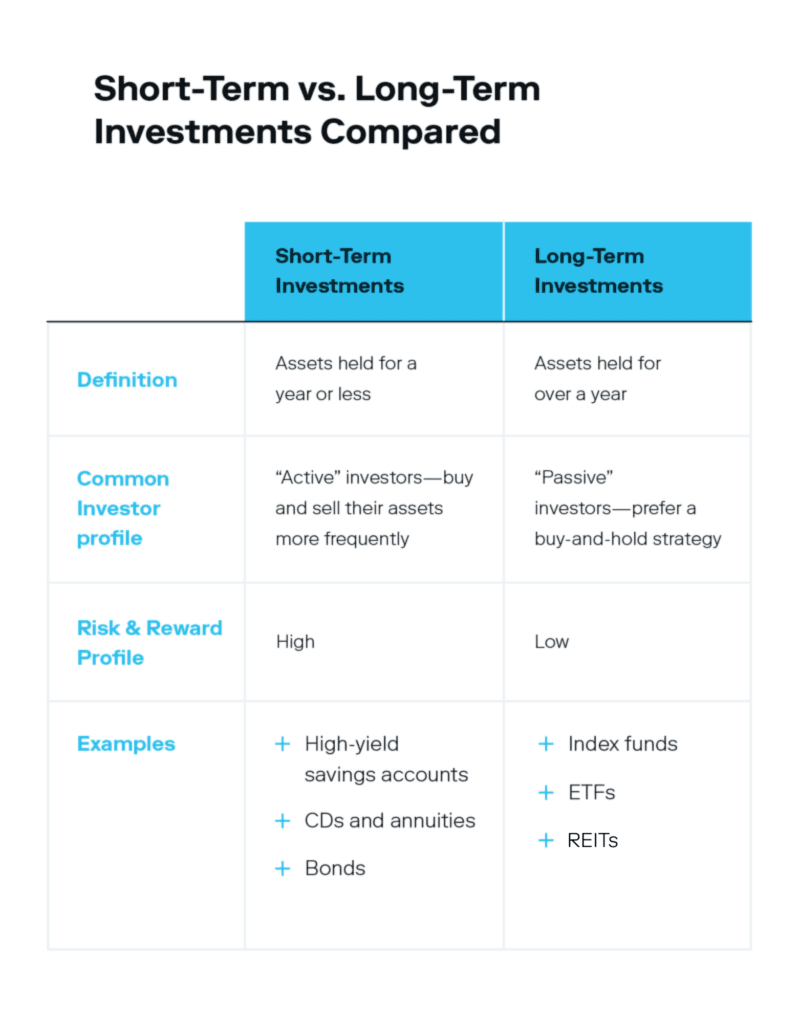

Short-term vs. long-term investing Short-term investing means holding an asset for a year or less, or even just a few weeks for many day traders. Long-term investing means holding an asset for a year or more, but many long-term investing strategies entail holding assets for 5–10+ years. |

|---|

Short-term vs. long-term investing refers to how you use different investments based on your financial goals and time horizon. The main difference between the two lies in how you approach an investment, not in the investment itself. Both short-term and long-term investments can include any asset class. A stock, for example, can be a short-term or long-term investment depending on how you use it, like buying and selling a stock within a single month versus buying and holding a stock for several years.

Once you know the difference between short-term and long-term investments, you can craft an investment strategy that moves the needle on your long-term wealth goals.

Now, let’s dive into those differences between short-term and long-term investments, and how to decide which is best for you and when.

Short-term investments explained

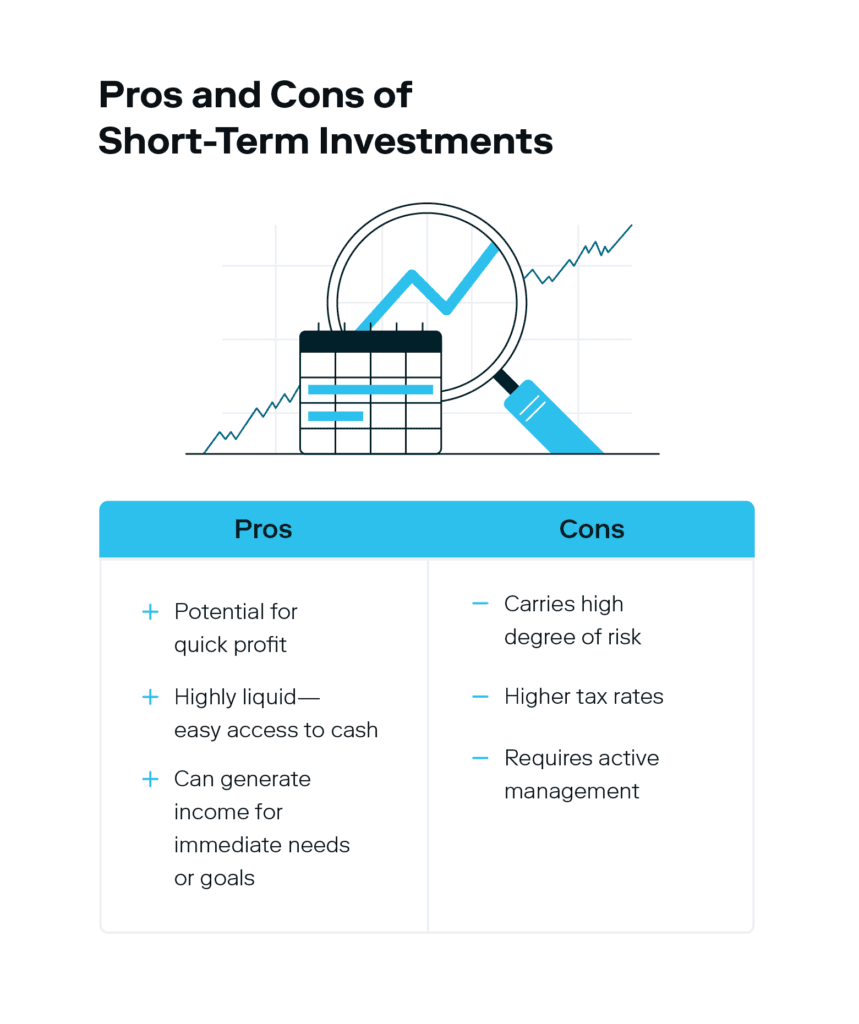

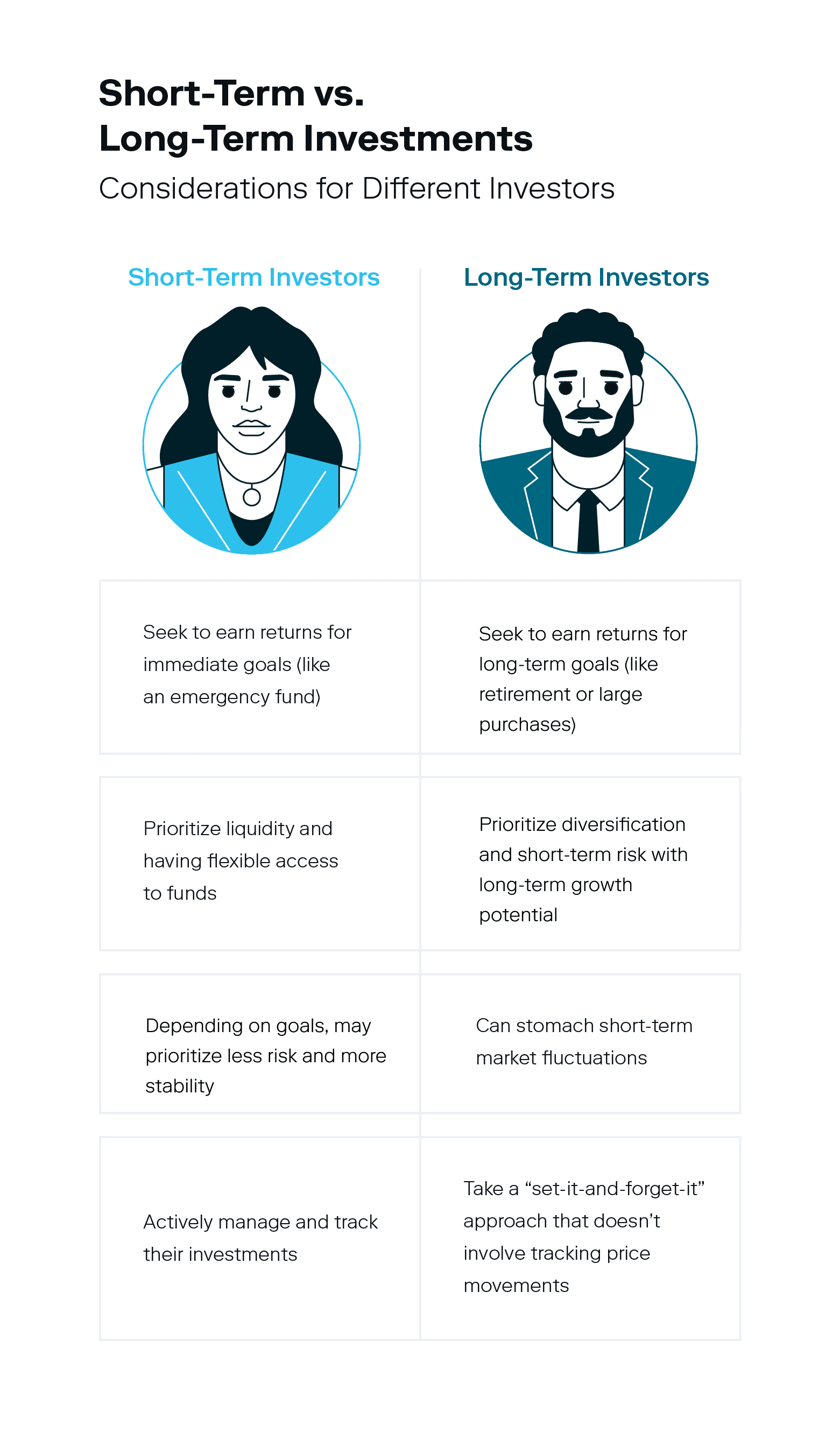

Short-term investments are assets held for less than a year, like certificates of deposit (CDs) or a stock options contract. They’re often favored by investors with financial needs or goals in the near future, like saving for a down payment on a home or car.

That said, there are different approaches to short-term investments depending on your goals and risk tolerance.

Short-term investors who trade options, for example, may buy and hold a stock for as little as a few weeks before selling it, with the goal of profiting from short-term price movements. Their goal is to turn a quick profit in a short period of time. While betting on short-term stock price fluctuations can provide outsized returns, it’s a highly risky and volatile short-term investing strategy.

On the other hand, risk-averse short-term investors looking for more stable returns may favor any of these common short-term investments:

High-yield savings accounts

CDs

Short-term bonds

Money market accounts

Compared to options trading, the investments above offer a less risky approach to short-term investing that can be used to grow your savings for an upcoming purchase.

Long-term investments explained

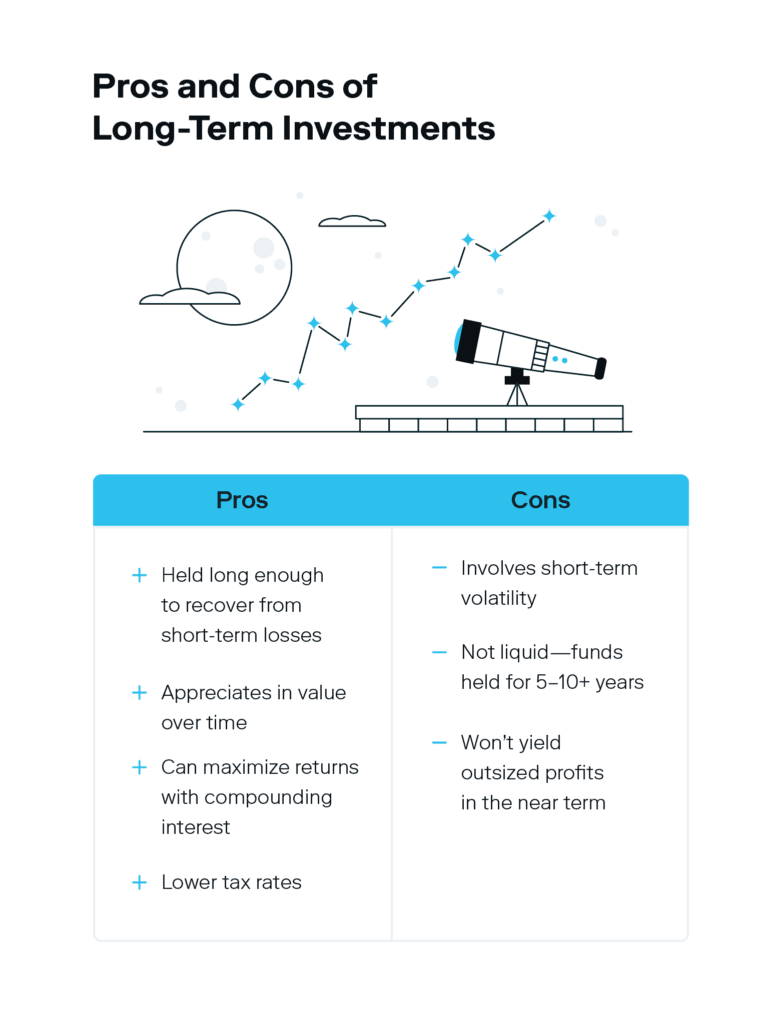

Long-term investments are assets held for at least a year or more, and are often used to fund long-term financial goals like saving for retirement. Long-term investors tend to invest with the expectation that their investment will appreciate in value over time, despite short-term volatility. Common long-term investments include:

While short-term investors keep a close eye on the day-to-day performance of their investments, long-term investors have time to recover any lost value that might occur in the short term. That’s because when you hold an investment for five or 10 years, short-term market fluctuations, bear markets, and even recessions have enough time to level out. (And historically, they always do.) An S&P 500 index fund, for example, yields an annual average return of 11.34% (1950-2023) when held long-term.

This makes long-term investments generally less risky than short-term investments, although the level of risk depends on the specific investment. Regardless of which investment you choose, they all share the same buy-and-hold strategy.

Investor tip: Whether you invest in an index fund, stocks, or a 30-year government bond, long-term investing means you plan to hold your asset for many years—even decades.

Short-term vs. long-term investments: Main differences

While the biggest difference between short-term and long-term investments is time, there are a few others to know, such as active versus passive investing.

Short-term investors are referred to as “active investors,” and some common attributes of a short-term investor include:

They buy and sell their assets more frequently (several times a year, month, or even in a single day).

They lean into high liquidity investments.

They spend more time watching the markets and tracking daily price movements (otherwise known as “timing the market,” a common strategy for short-term stock investments).

On the other hand, long-term investors are referred to as “passive investors,” and some common attributes of a long-term investor include:

They tend to invest with a buy-and-hold strategy.

They seek to avoid the risks associated with frequent short-term trading.

Rather than reacting to daily market fluctuations, they’re more focused on the big picture and how their investments can grow over time.

The characteristics investors seek in short-term vs. long-term investments also differ. Short-term investors who day trade usually make investing decisions based on things like low share prices, industry growth forecasts, and daily price movements. Short-term investors who aren’t looking to day trade but still want to reach a near-term investing goal within a year look for safer liquid investments that they can easily convert to cash, like a high-yield savings account.

Alternatively, long-term investors usually focus more on diversification, staying invested for the long haul, and utilizing established investing principles like favoring time in the market (as opposed to timing the market, like a day trader would).

What to consider when choosing short-term vs. long-term investments

Choosing between short-term vs. long-term investments ultimately depends on your time horizon, financial goals, and risk tolerance. But both may have a place in your portfolio. Here’s what to consider.

Investment goals and time horizon

Your investment goals are your north star for choosing the right investments, followed by your time horizon (that is, how soon you’ll need the money you’re investing). You’ll want to group your high-level financial goals into time horizons of near term and long term in order to choose the investments that make the most sense.

Investors with near-term goals often choose short-term investments. Day traders who rely on their short-term trading profits may have the goal of generating income for the next week or month. Not all short-term investors are day traders, though, and some may choose investment vehicles like a one-year bond or CD if their goal is to safely grow their savings for a particular upcoming expense, like a home down payment or a vacation.

Other short-term investments like high-yield savings accounts or money market accounts may appeal to investors who want more flexible access to their funds (since funds invested in bonds or CDs shouldn’t be touched until the term date is reached).

On the other hand, investors looking to achieve long-term goals will select long-term investments that won’t be touched for an extended period of time—even decades. Please note, long-term investments may not necessarily be locked up for a long period, and if you had an emergency you’d likely be able to access some of your investment. However, it is preferred that you hold long-term investments for an extended period in order to smooth out short-term price volatility and reap the reward of market growth over time.

Risk and volatility

Beyond assessing an investment’s potential returns, understanding the volatility of an asset over time can help you choose investments that align with your ideal risk tolerance.

For example, two funds that yield the same long-term returns may endure totally different levels of volatility along the way. To choose the right investment, whether short or long term, you should get clear on the amount of risk and volatility you can stomach. Risk-averse short-term investors may choose to grow their money safely through interest-bearing accounts like CDs—a very low-risk investment.

In general, investors with longer time horizons can assume more risk because they can stay invested long enough to weather any downturns. That’s why long-term investments like index funds are ideal if you’re still decades from retirement, even though they’ll likely experience short-term market fluctuations and volatility along the way.

Taxes

Finally, don’t forget about capital gains tax considerations—the tax you’re required to pay whenever you profit from the sale of any type of asset. For investments, these are categorized by long term and short term.

Short-term capital gains taxes apply to assets you owned for less than a year, and they’re taxed the same as regular income (like wages earned from a job), typically around 20%–35%. Long-term capital gains taxes apply to assets owned for a year or more, and are taxed between 0% and 20%, and often work slightly more in your favor—you’ll generally pay less in taxes on long-term capital gains versus short-term capital gains. Additional state taxes may apply.

Long-term capital gains are often favored due to their lower tax rate. Short-term investors who frequently buy and sell assets may eventually assume a higher tax liability that can erode their profits or eat into their earnings. That said, those short-term investments are still worth it to many investors when the returns are substantial enough.

While it can be easy to get lost in the minutia of analyzing different short-term vs. long-term investing tactics, keeping a big-picture view of your financial goals, risk tolerance, and time horizon is key to building a well-rounded portfolio. Also foundational to a successful investment portfolio is ensuring you’re properly diversified—for most investors, that means keeping a healthy mix of long-term and short-term investments.

Investing made easy.

Start today with any dollar amount.

FAQs about short-term vs. long-term investing

Lingering questions about short-term vs. long-term investments? We’ve got answers below.

Is it better to invest short-term or long-term?

It depends on your financial goals. If you want to grow your money for a purchase you know you’ll need to make in the near term, short-term investments allow you to do so in a shorter time frame. When it comes to high-level financial goals and saving for retirement, however, long-term investments are often the best option.

Are short-term investments better?

This depends on your financial goals. If your goals require near-term access to your savings and investments, then it’s important to select the appropriate short-term investments. However, if your goals are long-term in nature, then you can afford to be less risky with your investments and participate in the overall growth of the stock market over time. Many investors will have both short-term and long-term investments to meet the needs of multiple goals.

How long is a short-term investment?

From a capital gains tax perspective, short-term investments refer to assets held for one year or less. In regards to general personal finance, a time frame of three years or less may be used when identifying short-term investments.

How long is a long-term investment?

From a capital gains tax perspective, long-term investments refer to assets held for at least one year or more.

Written by

Team Stash

We want to turn money into a source of hope and opportunity. We teach people how to build good habits, save more and make it easy and affordable to get started investing. So far, we’ve helped over 6 million people create a more secure financial future with our expert advice and award winning investing app.

Related articles

investing

Jun 25, 2026

Should You Buy IPOs? 4 Myths About Hot New Listings

investing

Jun 18, 2026

Best Index Funds for Beginners and How to Pick One

investing

Jun 10, 2026

What Is an Index Fund? A Complete Beginner's Guide

investing

Jun 09, 2026

How to Start Investing: A Beginner’s Guide for 2026

investing

Jun 04, 2026

What Is Quantum Computing? An Investor’s 2026 Guide

investing

Jun 03, 2026

What Is an IPO? How It Works for Everyday Investors

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.