Should You Max Out Your Roth IRA? How Does $1.3M at 65 Sound?

Published: Feb 26, 2024

• Updated: Mar 16, 2025

In this article:

- What Is a Roth IRA?

- The Benefits of Maxing Out a Roth IRA

- What does it mean to max out your Roth IRA?

- 6 Reasons you should max out your Roth IRA

- When Should You Avoid Maxing Out a Roth IRA?

- When shouldn’t you max out your Roth IRA?

- How to max out your Roth IRA

- Real-Life Success Stories

- Max Out Your Roth IRA and Build Your Future

- When can you contribute to a Roth IRA in 2025?

- Frequently asked questions

To max out your Roth IRA, you must reach annual contribution limits—$7,000 a year or $8,000 when you turn 50. Maxing out a Roth IRA is often a good idea, but it may not make sense for everyone. |

|---|

Do you want to be a millionaire? Of course, who doesn’t?

Maybe it seems far-fetched, but it’s possible if you max out a Roth IRA. You might even be able to retire earlier than age 65. But even if you don’t start saving in your 20s or early 30s, you can still build quite the nest egg with this strategy.

Follow along to learn what it means to max out a Roth IRA, if this strategy is best for you, and how to get started.

What Is a Roth IRA?

To determine whether it’s worth maxing out your Roth IRA, it’s important to first understand the basics of what it is and how it works.

A Roth IRA (Individual Retirement Account) is a retirement savings account that offers tax-free growth and withdrawals. Contributions are made with after-tax dollars, meaning you don’t get a tax deduction today. However, when you withdraw your money in retirement, it’s completely tax-free—as long as you adhere to certain rules, like waiting until age 59½ and holding the account for at least five years.

Key Features of a Roth IRA:

Tax-Free Growth: Your earnings grow tax-free, and you won’t owe taxes upon withdrawal in retirement.

Contribution Limits: For 2024, you can contribute up to $6,500 annually ($7,500 if you’re 50 or older).

Income Limits: Eligibility phases out for individuals earning more than $153,000 or couples earning more than $228,000 (2024 limits).

Flexibility: You can withdraw contributions (but not earnings) without penalty at any time, making it somewhat flexible if you need access to your funds early.

Now that you understand what this investment tool offers, let’s explore why—or why not—it makes sense to max out your contributions.

The Benefits of Maxing Out a Roth IRA

Roth IRAs are especially beneficial for young professionals and long-term planners. Here are some reasons why maxing out your contributions annually could be a smart move:

1. Tax-Free Withdrawals in Retirement

One of the standout benefits of a Roth IRA is that you won’t pay taxes when you take the money out in retirement. For young professionals in lower tax brackets now, this is particularly appealing since your earnings over the next few decades can grow entirely tax-free.

2. Compound Growth Over Time

By contributing the annual maximum of $6,500 consistently, you’re giving your money the best opportunity to grow. For example, if you start maxing out your Roth IRA at 25, with a 7% annual return, your investments could grow to over $1 million by age 65. That’s the power of compounding.

3. No Required Minimum Distributions (RMDs)

Unlike a Traditional IRA or 401(k), Roth IRAs don’t require you to take distributions at a certain age. This gives you more control over your savings and allows your money to keep growing uninterrupted.

4. Diversification of Tax Strategy

By paying taxes now (when your income is likely lower), you reduce your tax burden later. This tax diversification can be a lifesaver when creating a more balanced strategy for retirement withdrawals.

5. Flexibility in Saving

Unlike other retirement accounts, Roth IRAs allow you to withdraw your contributions penalty-free at any time. While it’s not advisable to dip into your retirement savings early, it’s reassuring to know you have options in case of an emergency.

6. Exclusive Subscriber Advantages

Beyond just retirement, if you pair your Roth IRA with resources like Stash, you’re tapping into practical financial tools that make long-term investing feel accessible, not overwhelming.

What does it mean to max out your Roth IRA?

Maxing out your Roth IRA means contributing the maximum amount the IRS allows annually. In 2024, this means stashing away $7,000 yearly or $8,000 if you’re 50 or older.

While maxing out isn’t complicated, it’s not attainable or wise for everyone. We’ll cover when you shouldn’t max out your Roth IRA later.

Pros | Cons |

|---|---|

You may accumulate savings upward of $1.3M for retirement (calculated with a 7% rate of return and a savings time horizon of 40 years). | Contributions are not tax deductible |

Tax-free qualified withdrawals and no requirement to withdraw | Some financial goals may be more important to check off, like making contributions to your employer 401(k) that qualify for a matching contribution |

You can lock in taxes at your current tax rate | No employer matching |

Roth IRAs offer a wide range of investment types | 6% penalty tax for over-contributing |

It’s easier to max out your Roth IRA over a 401(k) | If you fall into a lower tax bracket when you retire, you may have paid more in taxes initially |

You can pass a Roth IRA to heirs | Income limits restrict who qualifies to make a Roth IRA contribution |

6 Reasons you should max out your Roth IRA

If you’re able to, maxing out your Roth IRA is generally a good idea. But it’s wise to be informed before you make any financial commitment. To help you decide, we’ve outlined the benefits of maxing out a Roth IRA for you below.

1. You’re setting yourself up for retirement

The obvious reason for maxing out your Roth IRA is to set yourself up for a comfortable life in retirement.

Roth IRAs are a long-term investment, meaning you shouldn’t plan to access your Roth IRA savings in the short term. You may not even be able to touch earnings during a defined period without facing a penalty.

It may seem unrealistic to put away a significant chunk of your salary for a time in your life that’s so far away. But if you continue to max out your contribution each year, your total investment may grow to be larger than your contributions. The rest is all tax-free earnings that have grown over time, and you can use it however you want.

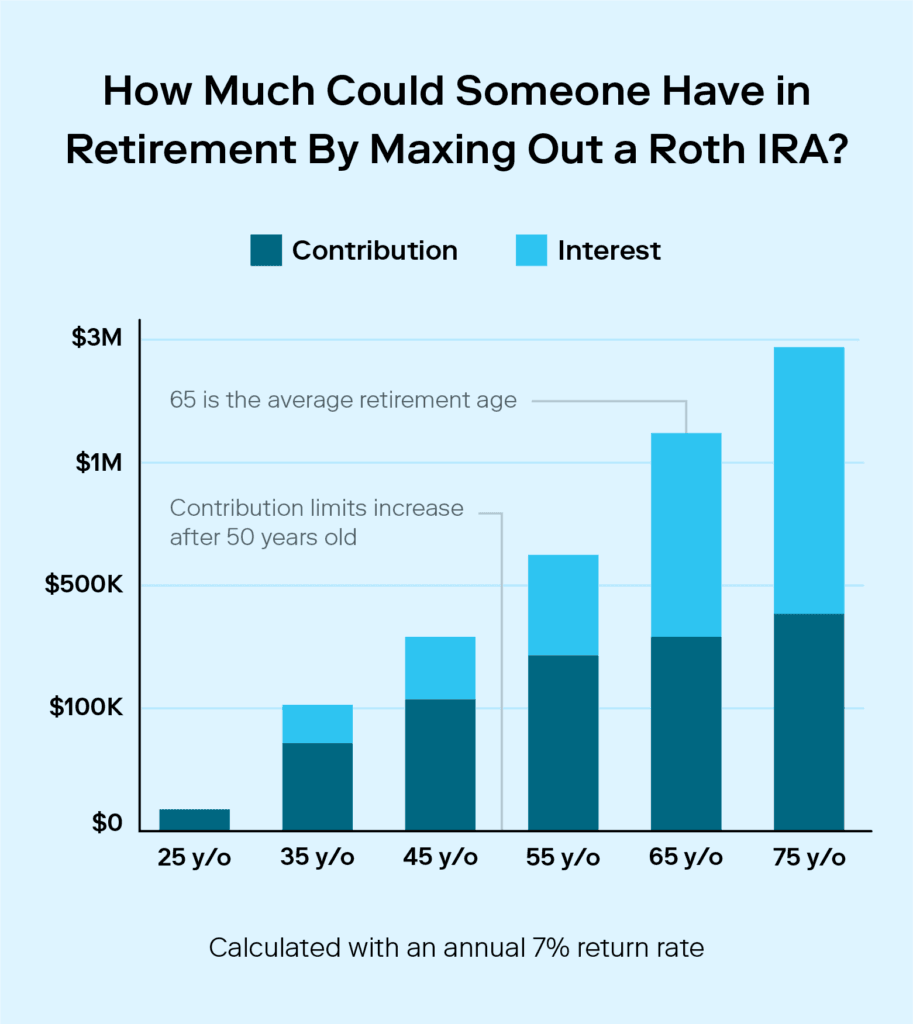

The chart below shows hypothetically how much someone could have in their Roth IRA if they started maxing out their contributions at age 25. We calculated the results with an annual 7% return rate. Though the chart starts at age 25, it’s never too early (or too late) to open a Roth IRA.

This chart hypothetically illustrates how investments may impact the long-term value of investing in the market, assuming an annual growth rate of 7% (compounded annually). This is purely an illustration of mathematical principles, and such results do not represent actual investing results and do not take into consideration fees, taxes, other account deposits, dividend reinvestment, time horizon, or economic factors which can impact performance. Diversification, asset allocation, and dollar cost averaging does not ensure a profit or guarantee against loss. Clients may achieve investment results materially different from the results portrayed. This example is for illustrative purposes only and is not indicative of the performance of any actual investment or investment strategy.

2. There are no withdrawal requirements

Some retirement accounts, like traditional IRAs and 401(k)s, have required minimum distributions (RMD). After you turn 72, you must withdraw a percentage from the account each year, even if you don’t need the cash (such withdrawals may be subject to ordinary income tax rates). Roth IRAs don’t have RMDs (unless passed on to an heir), meaning you can let it grow even after you retire.

If you need money before retirement, you can withdraw from your Roth IRA contributions without penalty. This is a benefit should you ever need a backup on your emergency fund—but it should only be used as a last resort. Withdrawing from Roth IRA earnings early is hit with a 10% tax penalty.

3. You can benefit from the current tax rate

With a Roth IRA, you pay taxes on your investment when contributing funds, not when you withdraw. Tax rates are ever-changing, so you can benefit from your current tax rate by maxing out a Roth IRA now. Your Roth IRA withdrawals won’t be touched if tax rates increase or you retire in a higher tax bracket.

Contributing post-tax dollars also gives you a clearer picture of how much money you will retire with since there will be no withdrawal penalties after age 59 ½.

4. You may have wider access to investment types

Compared to some employer plans, you may have access to a broader range of investment types with a Roth IRA, making it an ideal choice to max out. With an employer plan, you are subject to the investments they offer. Since you can set up a Roth IRA, you have free range to select whichever you’d like—from stocks to index funds and more.

In further comparison, you may find higher expense ratios on employer-run retirement plans.

INVESTOR TIP: If offered, you should prioritize reaching your employer’s 401(k) matching limit before maxing out a Roth IRA. Employee contributions are extra money, so take advantage of the benefit.

5. It’s easier to max out your Roth IRA over a 401(k)

If you’re comparing a Roth IRA to a 401(k) from a numbers perspective, it’s easier to max out a Roth IRA over a 401(k). It comes down to contribution limits. Roth IRA contribution limits are $7,000 a year or $8,000 if you’re 50 or older. 401(k) contribution limits are much higher at $23,000 or $30,500 if you’re 50 or older. The Roth IRA’s lower contribution limit is more attainable to max out.

6. You can pass it on to heirs

Maybe you’re thinking, “Will I really use a million dollars in retirement?” If you live a frugal life, maybe you won’t. But another major bonus of a Roth IRA is that it can be inherited. If you pass with money left in your Roth account, your beneficiary will be thankful that you maxed out your contributions.

Roth IRAs work slightly differently once passed on to heirs, though. Beneficiaries don’t pay additional taxes on withdrawals on inherited IRAs. However, most require beneficiaries to withdraw the money within 10 years and meet RMD obligations.

When Should You Avoid Maxing Out a Roth IRA?

While maxing out a Roth IRA can be a great financial move, it isn’t for everyone. Here are scenarios where it might not make sense to prioritize this account:

1. You Have High-Interest Debt

If you’re carrying high-interest debt (like credit cards), it’s smart to put your extra money toward paying it off first. The returns you’ll gain from avoiding interest far exceed the benefits of investing in a Roth IRA.

2. You Haven’t Built an Emergency Fund

Financial safety comes first. Before maxing out a Roth IRA, ensure you have at least 3–6 months’ worth of living expenses saved in a high-yield savings account for unexpected situations.

3. Your Employer Offers a Match

If your employer offers a 401(k) with a match, it’s advisable to contribute at least enough to maximize that benefit before focusing on a Roth IRA. Free money is hard to beat!

4. You’re Close to the Income Limit

If you’re nearing the income threshold that disqualifies you from contributing to a Roth IRA, it may be worth exploring the backdoor Roth IRA strategy to remain eligible.

When shouldn’t you max out your Roth IRA?

In some scenarios, maxing out a Roth IRA might not be the best investment decision. Some financial goals worth prioritizing over an IRA include:

Building an emergency fund

Saving for a specific event, like buying a house or paying off debt

401(k) contributions to meet employer matching limits

Additionally, if you expect to be in a lower tax bracket when you retire, consider skipping a Roth IRA altogether. Instead, you can max out a traditional IRA.

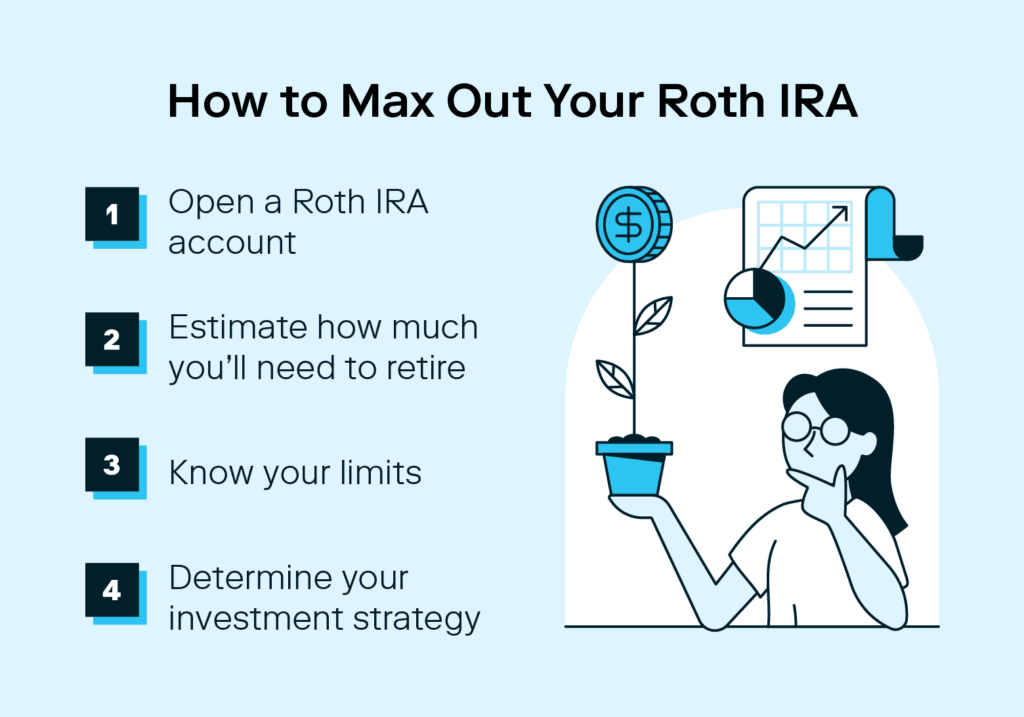

How to max out your Roth IRA

Ready to maximize your retirement savings with a Roth IRA? Here are four simple steps on how to max out your Roth IRA.

1. Open a Roth IRA

Before starting a Roth IRA, you should consider which type of provider is best for you—an online broker or robo-advisor. If you’re savvy with investing and want to manage your assets yourself, opt for a broker. If you want to be hands-off, have a robo-advisor automatically invest and handle your account.

You can open a Roth IRA in a matter of minutes with Stash.

2. Estimate how much you’ll need to retire

Even if you plan to max out your Roth IRA, you should still calculate how much money you’ll need in retirement to determine if your IRA will meet your needs.

To do so, use a retirement calculator to determine how much you’ll need to retire by your ideal retirement age. This can indicate whether you should make additional investments or if your Roth IRA will suffice.

3. Know your limits

Don’t dive into maxing out your Roth IRA without knowing how it will affect your finances in the short term. While you want to live a comfortable life in retirement financially, you don’t want to struggle now, either.

Analyze your bank account to better understand whether you can afford to max out your Roth IRA. Then, create a budget to ensure you can still pay your bills and remain secure in your finances.

4. Determine your investment strategy

Once you have the account and a financial plan, you’re ready to select your Roth IRA investment strategy. If you opt for a robo-advisor, your contributions will be invested based on your risk tolerance. Otherwise, consider a mix of assets, such as bond index funds, growth stocks, and the S&P 500. A diversified portfolio helps mitigate investment risks.

Next, you’re ready to make contributions. You can contribute monthly, in one lump sum each year, or in whatever manner works best for you. If your financial situation changes and you can no longer keep up with maxing out your Roth IRA contributions, you can dial it back temporarily. Please note, while the annual maximum contribution for a Roth IRA is $7,000 for those under age 50, and $8,000 for those age 50 or above, you still have to have earned income in order to qualify to make a Roth IRA contribution. Your contribution limit is also capped at the amount of your earned income. So if you only earned $4,000 of income this year, then the maximum you can contribute is limited to $4,000. Some people may wait to make a Roth IRA contribution until the end of the year to understand their earned income total if they’re not sure if they’ll have enough to contribute the maximum amount allowed.

Separate from your Roth IRA, you should determine if you’ll need supplemental investments. You may have uncovered gaps between what you’ll need in retirement and the combination of your employer-sponsored plans and maxed-out IRA. In this case, you’ll want to plan how to address that difference. Investing in real estate, for example, might be a good option for you to bring in extra income in retirement.

Frequently asked questions

Still unsure if you should max out your Roth IRA? Let us help.

Is it worth maxing out your Roth IRA?

Yes, it is worth maxing out your Roth IRA as long as reaching contribution limits won’t put you under financial stress now. The pros outweigh the cons in this scenario.

However, if your employer offers contribution matching, prioritize contributing to your 401(k) first, but only up to their matching limit. Then with your remaining budget, contribute to your Roth IRA.

Can you max out multiple Roth IRAs?

While you can have many Roth IRA accounts, you cannot max out more than one IRA—Roth or traditional. Contribution limits cover all IRA accounts you may have. In 2024, the total contributions between all your IRAs can’t exceed $7,000, or $8,000 if you’re over 50.

If you exceed the contribution limit and don’t correct the error by the year’s end, you will be subject to a 6% penalty from the IRS.

Should I max out my 401k or Roth IRA first?

If your employer offers to match your 401K contributions, prioritize matching up to the limit your employer will contribute before maxing out your Roth IRA. It’s important to take advantage of the benefits you’re offered and employee matching gives you extra money.

Can you max out your Roth IRA contribution at one time?

If your financial situation allows for it, you can max out your Roth IRA in one lump-sum. This strategy can let you take advantage of potential investment growth over time. However, investing smaller amounts regularly over time can help mitigate the impact of market fluctuations. This is known as dollar cost averaging.

What to do when you max out your Roth IRA?

If you have maxed out your Roth IRA before the end of the tax year, there are other retirement investment account types you can turn to instead of pocketing the cash. You can:

Increase your 401(k) or 403(b) contributions

Contribute to a Roth 401(k) if your company offers it

Invest in a spousal IRA if applicable

Real-Life Success Stories

Emma, 28

Emma started maxing out her Roth IRA at 25 while earning $45,000 a year. By automating her contributions and investing in target-date funds, she’s already on track to surpass $750,000 in retirement savings.

Mike, 37

Mike used his Roth IRA not just for retirement but for flexibility. When he faced unexpected medical expenses, he was able to withdraw contributions penalty-free, proving the account’s versatility.

Max Out Your Roth IRA and Build Your Future

Maxing out your Roth IRA is one of the smartest moves young professionals and retirement planners can make. It’s a tool that goes beyond saving—it helps you build financial freedom.

However, it’s equally important to evaluate your current financial situation. High-interest debt, a lack of emergency savings, or missing out on employer-matching contributions might mean waiting to max out until you’re in a stronger position.

Take control of your financial future on your terms. Platforms like Stash make it easier than ever to manage your investments without the overwhelm.

Start small, grow big, and see your wealth take shape.

When can you contribute to a Roth IRA in 2025?

You have until Tax Day every year to contribute to your Roth IRA for the year prior. So for 2025, you can work toward maxing out your Roth IRA until April 15, 2026. Each January 1, you can contribute to the new year’s IRA. However, focus on maxing out the prior year’s contributions before contributing to the new year’s.

Investing made easy.

Start today with any dollar amount.

Written by

Team Stash

We want to turn money into a source of hope and opportunity. We teach people how to build good habits, save more and make it easy and affordable to get started investing. So far, we’ve helped over 6 million people create a more secure financial future with our expert advice and award winning investing app.

Related articles

taxes-and-retirement

Jun 10, 2026

What Is a Backdoor Roth IRA and How It Works in 2026

taxes-and-retirement

Jun 10, 2026

Roth Conversion Explained: Taxes, Rules, and Timing

taxes-and-retirement

Jun 06, 2026

Roth IRA vs Traditional IRA: Which Fits Your Taxes

taxes-and-retirement

Jun 06, 2026

Roth IRA Contribution Limits 2026: Key Rules to Know

taxes-and-retirement

Jun 06, 2026

What Is a Roth IRA? Rules, Taxes, and Who Qualifies

taxes-and-retirement

Dec 15, 2025

FAQ: Retirement Portfolio

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.