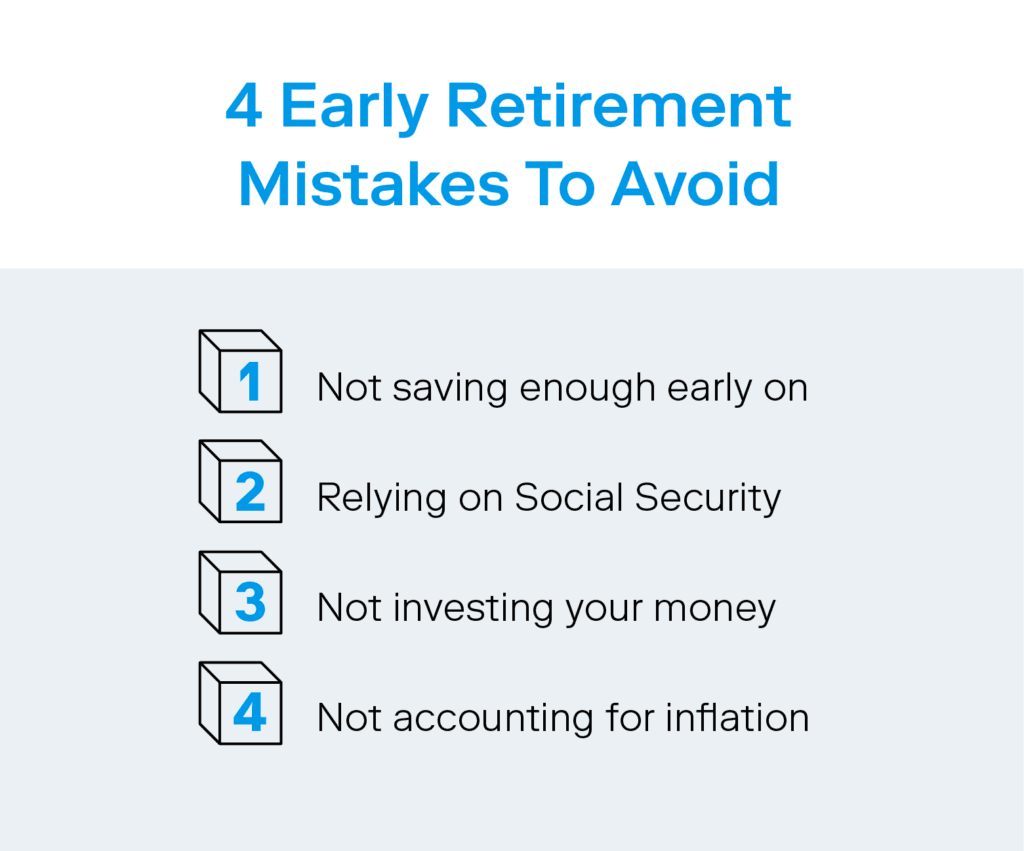

How To Retire Early: 7 Steps To Plan For Early Retirement

Published: Aug 12, 2023

• Updated: Jun 09, 2026

In this article:

- 1. Envision your ideal lifestyle during retirement

- 2. Make a draft retirement budget

- 3. Know your current financial standing

- 4. Level up your investments

- 5. Assess your current lifestyle for savings opportunities

- 6. Identify your fixed income streams—and know how to manage them

- 7. Enlist the help of a financial advisor

“How can I retire early?” That question might not keep you up at night if you’re still riding out your 20s—but if you like the idea of cutting down your working years and enjoying more financial freedom later in life, now is the time to explore your options for how to retire early.

So what does it take to retire by the age of 55, or even 45? Knowing the average retirement savings by age can help set benchmarks for you, but the answer to how much you actually need depends on your unique circumstances and financial situation. There are a number of steps you can take if you’re serious about learning how to retire early.

To that end, consider this your ultimate how-to-retire-early guide.

1. Envision your ideal lifestyle during retirement

Before diving into nitty-gritty financial considerations, spend some time envisioning the type of lifestyle you want to lead in retirement. This will inform the concrete plan and budget you’ll need to support the life you envision.Maybe you want to spend time traveling abroad or buy a vacation home. Whatever your dreams are, get clear on the cost considerations associated with each. Figuring out the best way to retire early starts with affirming your ideal lifestyle during that time.

Be sure to consider key future life events, too. If you’re planning to move to a new state, for example, factor in cost-of-living differences for that city. Will you want to live near family or future grandchildren? Will that require you to move? Thinking about these things ahead of time will help you make more informed decisions when crafting your retirement budget.Here are some common key life events to consider:

World travel

Starting a business post-retirement

Committing to volunteer work

Moving to a new city or state (or country!)

Funding your kids’ or future kids’ college education

Caring for aging parents

Investor Tip: Retirement planning isn’t just a numbers game. A successful transition into your retirement years includes defining your ideal purpose or vision for those years of your life. |

|---|

2. Make a draft retirement budget

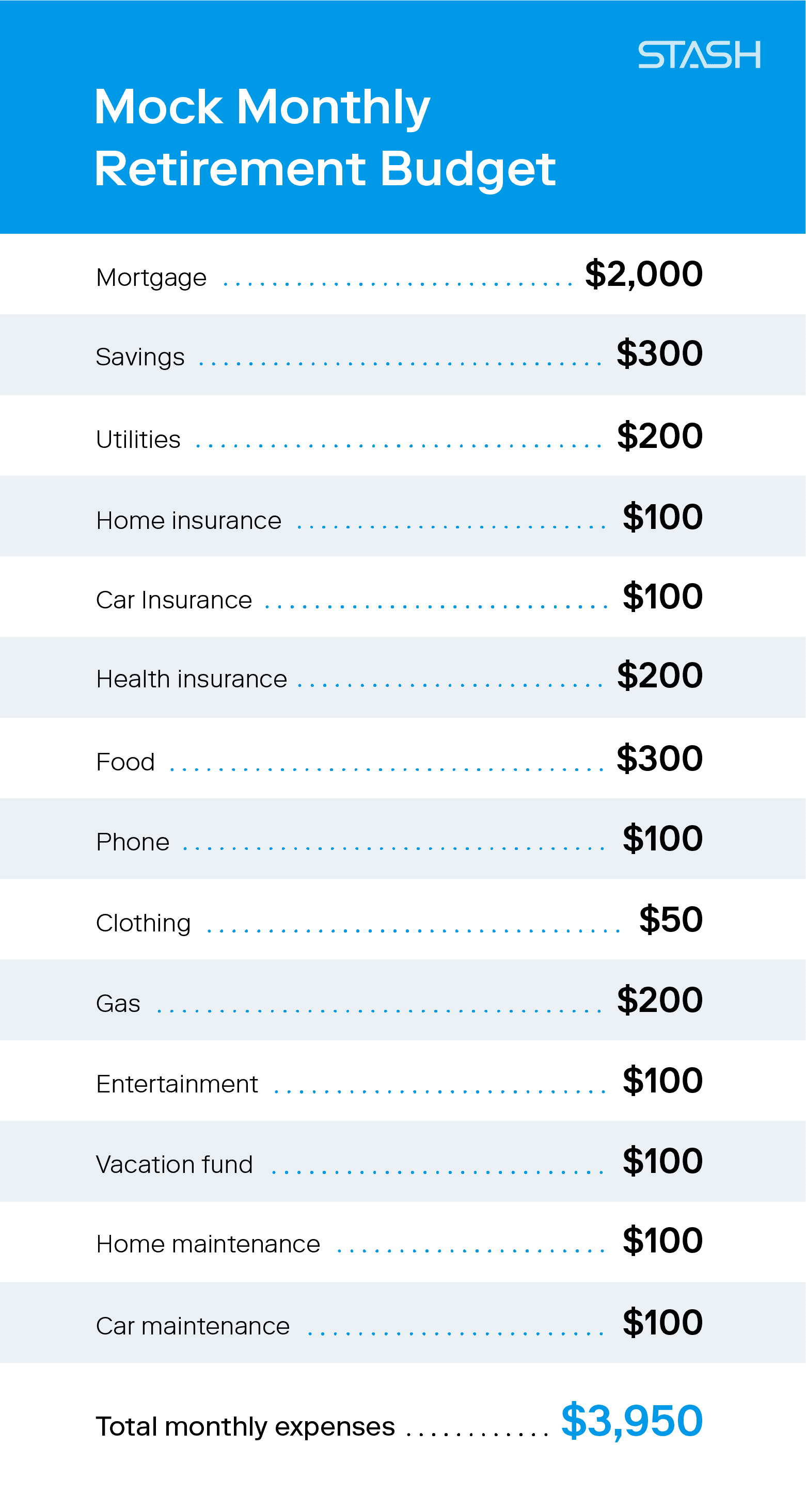

An important aspect of early retirement planning is getting specific about the projected budget you’ll need to live off when the time comes.An easy way to do this is by creating a mock monthly retirement budget to determine how much money you’ll need to live off each month.

Investor Tip: Many people use the 80% rule as a starting point—using 80% of your pre-retirement income as an estimate for how much you’ll need annually. |

|---|

Then, list your expected monthly spending. Many of your expenses will stay more or less the same in retirement, so take a look at your current costs (food, utilities, medical, insurance, internet, car, etc.) and use those numbers as a baseline.Adjust each item as needed based on your personal retirement goals. For example, if you know you want to buy a new car for retirement, estimate the monthly payments required for the new car versus the one you currently have.

It’s also important to plan for medical expenses during retirement. Medicare eligibility doesn’t go into effect until the age of 65, no matter when you retire. Unless you know your employer allows you to keep your current health plan after retirement, you’ll need to have a plan in place for where you’ll get health insurance and how much it will cost. For many, this might mean buying private insurance, which can greatly impact your overall budget.

3. Know your current financial standing

If your goal is to retire early, you need to take stock of where you currently stand financially and how far you have to go.Be sure to assess the following areas when evaluating your current financial standing:

Emergency fund savings

Outstanding debts

Mortgage payments

Contributions to retirement accounts (Roth IRA or 401(k))

If you’re 40 and want to retire in the next five years but only have $30,000 stashed in savings, you might struggle to have sufficient funds by the time you hope to retire.Assessing your current financial situation provides crucial insight into the true feasibility of early retirement, revealing any adjustments you might need to make or goals you should work more aggressively toward (like paying off debt) to make it happen.

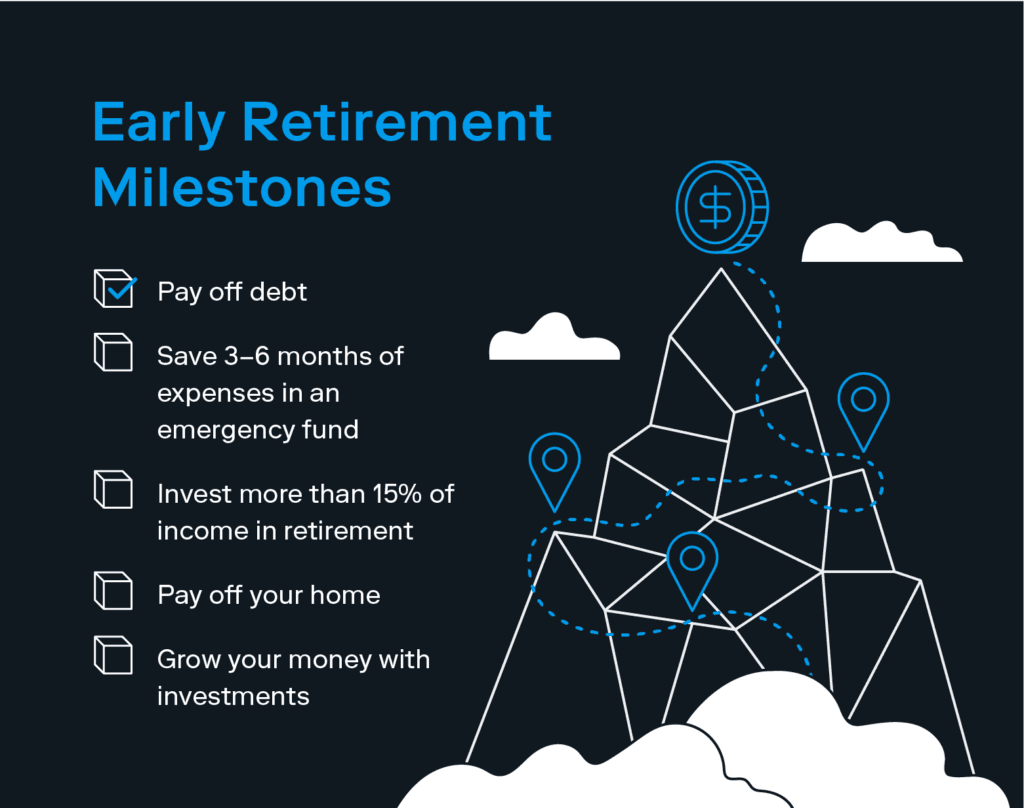

4. Level up your investments

Once you’ve taken action on your existing long-term wealth goals—like paying off debt, having a robust emergency fund, and paying off your mortgage—you should ideally be investing at least 15% of your income for retirement.

Curious how much you’ll need to retire?

Try our retirement calculator.

But if your goal is to retire early, you’ll want to find ways to put more dollars toward that goal—especially if you’re utilizing tax-advantaged retirement accounts like 401(k)s or IRAs, since those funds can’t be withdrawn until you’re 59 ½ (unless you want to pay a hefty early withdrawal fee).

So how do you fund the gap between early retirement and when you can begin to lean on your retirement accounts? By utilizing returns from other investments!

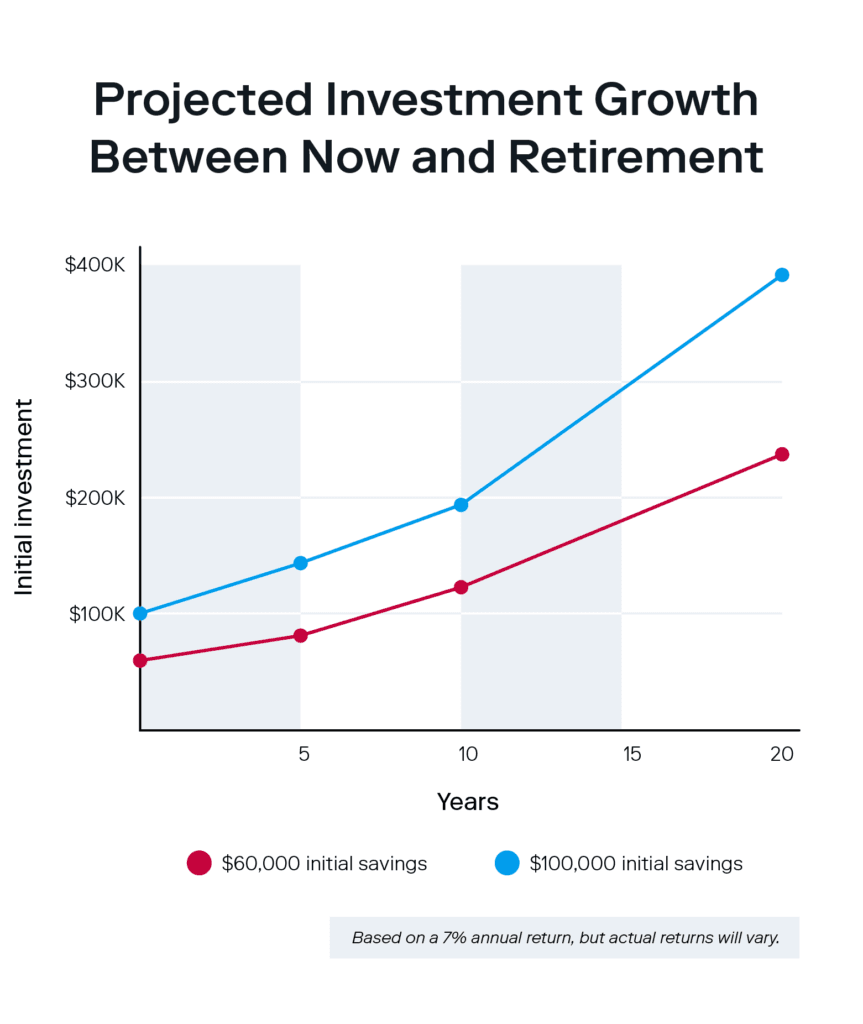

Once you’re contributing the maximum amount to your 401(k) or IRA, expand to other investments like exchange-traded funds (ETFs) to create a portfolio positioned for long-term growth. An ETF can passively track an existing index (like the S&P 500), making it a lower-cost option (as opposed to an actively managed mutual fund) that can compound your money over time.

You might think that a shorter time horizon until retirement means you should make less risky investments. But remember to account for the years you’ll spend in retirement—ideally, your money will continue to grow during this time.

When your retirement date draws near, you can plan to incrementally withdraw funds as needed, while also adjusting your risk levels down to mitigate short-term losses in periods of downturn. For example, you may allocate your taxable investments more conservatively while still contributing the maximum to your 401(k)s/IRAs. That’s because the investment funds you’ll be withdrawing—your taxable investments—are still subject to market fluctuations, so you’ll want to adjust your portfolio allocations accordingly.

When your retirement date draws near, you may plan to cash out on a year or two’s worth of those compounded funds so you have access to more liquid savings. If this is the case, leave the remaining funds invested—simply cash out funds as needed and let the rest compound over time.

Investor Tip: Passive investments offer an alternative path to early retirement, such as real estate or rental property investing. However, it’s smart to avoid jumping into real estate investing until you’ve paid down all of your debt, paid off your home, have a fully funded emergency fund, and have maxed out your monthly tax-advantaged retirement account contributions. |

|---|

5. Assess your current lifestyle for savings opportunities

The earlier you retire, the longer the length of time you’ll need to fund. One of the best tips to retire early is to be honest about what sacrifices you need to make now so you can realize that goal. It all depends on how early you want to retire and what you’re willing to do now to make it happen.

For instance, can you table your annual family vacation and invest the extra funds instead (or even just cut your vacation budget in half)? Or maybe you buy a used car in full instead of paying a monthly lease for the brand-new model you wanted.

Whether you make drastic cuts to your budget or simply stash away an extra $100 a month is up to you—just know that how much you put away now directly affects how quickly you can reach early retirement.

6. Identify your fixed income streams—and know how to manage them

Managing your income during early retirement requires understanding how much money you have and when you can take that money out.Your income streams are anything besides your emergency fund, such as:

401(k)s or IRAs

Cash

Real estate investment funds

High-yield bonds

Any other investments you have, like ETFs or mutual funds

If you’re retiring early, you’ll need to be strategic when it comes to planning your cash flows, since certain accounts don’t allow you to start receiving funds until you reach a certain age. The earliest you can claim Social Security benefits, for example, is age 62. And even then, you’ll only receive partial benefits, since full benefits aren’t offered until you reach age 65–67.

The rules and regulations for different accounts all vary. A financial advisor can be a valuable resource in ensuring you understand the timing and stipulations of yours.

7. Enlist the help of a financial advisor

While realizing your early retirement goals is ultimately in your hands, enlisting the help of a professional is a smart move. You don’t want to make a wrong move and realize you didn’t time your savings correctly or be forced to pay hefty fees because you didn’t understand the stipulations of certain accounts. A financial advisor can answer your questions and provide advice that’s in your best interest.

The answer to how to plan for early retirement is nuanced, but the steps above can expedite the process regardless of your financial standing.

And if you’re looking for further support, an investing platform like Stash not only makes it easy to invest what you can afford, but also provides all the personalized financial education you need to move the needle on your long-term wealth goals.

Learning how to retire early is one thing, but committing to making it happen requires some dedication. While early retirement isn’t for the faint of heart, it’s certainly possible if you’re committed to saving and know how to invest and grow your money over time—especially if you start early!

Investing made easy.

Start today with any dollar amount.

Written by

Team Stash

We want to turn money into a source of hope and opportunity. We teach people how to build good habits, save more and make it easy and affordable to get started investing. So far, we’ve helped over 6 million people create a more secure financial future with our expert advice and award winning investing app.

Related articles

taxes-and-retirement

Jun 10, 2026

What Is a Backdoor Roth IRA and How It Works in 2026

taxes-and-retirement

Jun 10, 2026

Roth Conversion Explained: Taxes, Rules, and Timing

taxes-and-retirement

Jun 06, 2026

Roth IRA vs Traditional IRA: Which Fits Your Taxes

taxes-and-retirement

Jun 06, 2026

Roth IRA Contribution Limits 2026: Key Rules to Know

taxes-and-retirement

Jun 06, 2026

What Is a Roth IRA? Rules, Taxes, and Who Qualifies

taxes-and-retirement

Dec 15, 2025

FAQ: Retirement Portfolio

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.