How to profit from inflation: best inflation investments to know

Published: May 30, 2024

• Updated: Aug 28, 2024

If you’re wondering why your grocery bill seems higher than usual even though you’re buying the same foods, this is just one of the many real-life examples of inflation in action. In addition to the cost of goods and services going up, inflation can hurt people and the broader economy in a number of ways—particularly when it comes to your investments.

While there’s no way to know for sure when inflation stabilize fully, you don’t have to avoid investing during inflation. In fact, it’s a great opportunity to revisit your portfolio to ensure you’re maintaining the value of your investments.

In this article, we’ll break down the best investments to consider if you’re eager to learn how to protect against inflation.

Keep reading to learn about the following best inflation investments:

TIPS

Real estate

Commodities

I-bonds

Value stocks

Now, let’s get into how to profit from inflation.

How inflation works

Inflation is the rate at which prices for goods and services increase over a period of time, expressed as a percentage.

Inflation is the rate at which prices for goods and services increase over a period of time, expressed as a percentage.

And inflation is normal. It’s why a gallon of gas cost $0.90 on average in 1987, but now goes for $3.59 as of May 2024.

One of the most common metrics measuring inflation is the Consumer Price Index (CPI), which is a measure of the average price urban consumers pay for goods and services. You can find it reported monthly by the Bureau of Labor Statistics (BLS).

A low, stable rate of inflation is around 2%, but that number can fluctuate significantly. For example, the 1970s and ’80s saw inflation of 10%–15%, which eventually leveled out to a more stable rate of 0%–2% in the 2010s. That number has shot back up in recent years, however—following the COVID-19 pandemic, inflation stood at 5.3% in September 2021, which was three times higher than it was in 2020. In June 2022, inflation rose to a whopping 9.1%, averaging an annual inflation rate of 6.5% for 2022.

And while inflation rates began to stabilize comparatively in the latter half of 2023 at an annual rate of 3.4% and have maintained this average in 2024, inflation is still high and a variety of factors can impact this current rate.

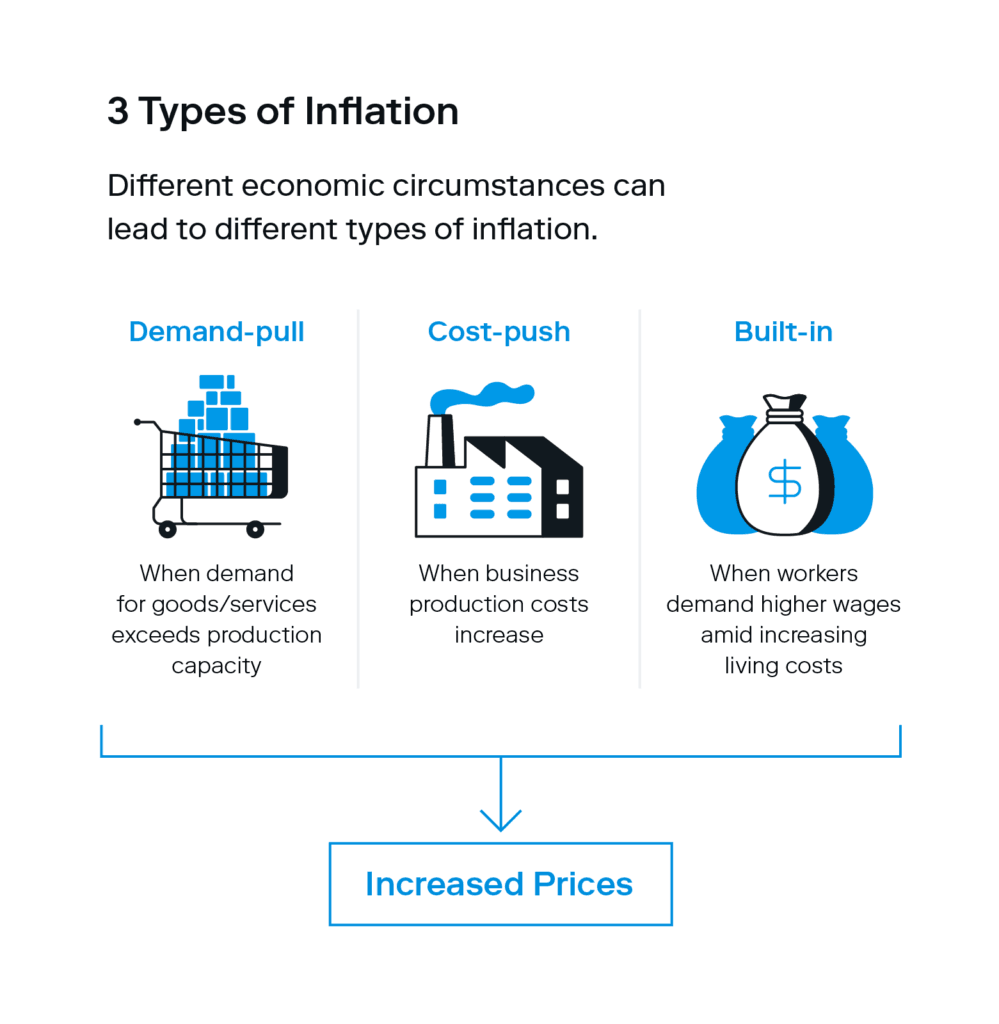

Inflation can be caused by a variety of factors, such as higher demand for goods and services or production shortages.These are the three main types of inflation:

Demand-pull inflation: Demand-pull inflation is when demand increases to a pace that supply can’t keep up with, resulting in increased prices.

Cost-push inflation: Cost-push inflation is when business production costs (the price of raw materials or workers’ wages) increase and consumer prices are increased to make up for the extra costs.

Built-in inflation: Built-in inflation is when workers demand higher wages amid increasing living costs. This can cause a feedback loop of companies raising prices in response to increasing labor costs.

No matter what type of inflation the economy faces, they can all impact you and your finances—the next section explains how.

How inflation affects your money

While the impacts of inflation can’t always be predicted, history can give us some general understanding of what to expect.

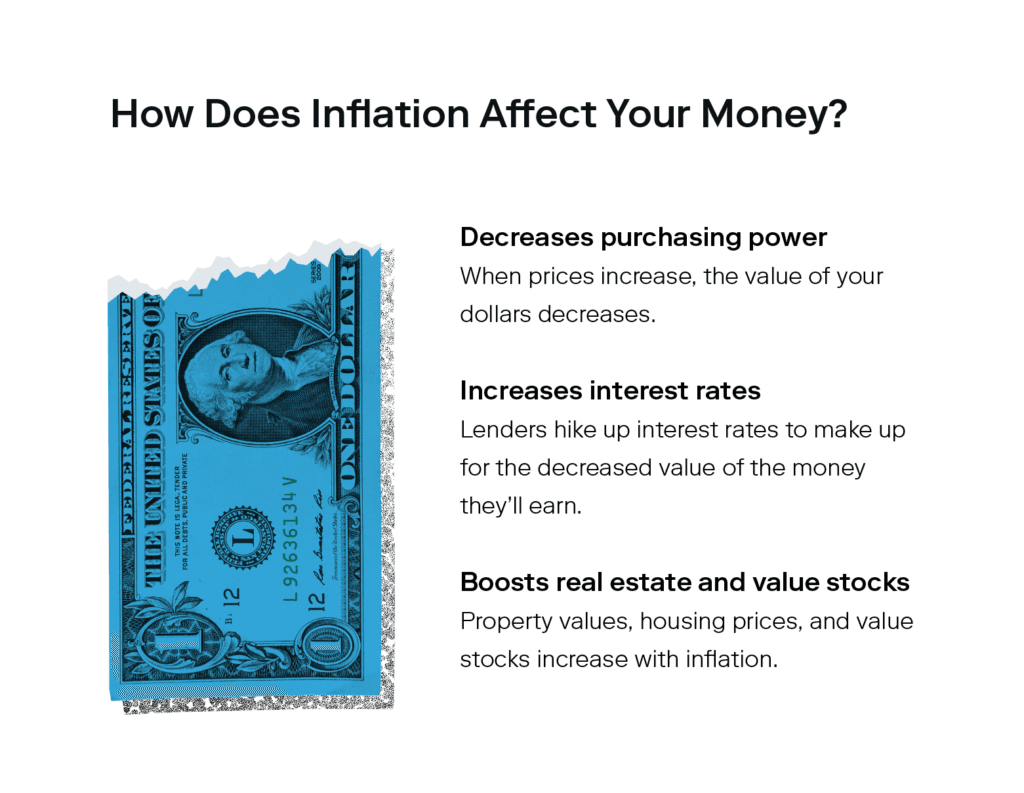

Decreases purchasing power

You’re likely already familiar with the most immediately noticeable effect of inflation. That is, price increases for goods and services. When prices increase, purchasing power decreases, meaning the value of your dollars is less than it was pre-inflation.

For example, if the inflation rate is currently at 3.4%, you’ll need $1.03 next year to buy what you could for $1 today.

This also applies to money you have put in savings accounts. For instance, say the money in your savings account grows at 1% yearly, but inflation is 4%. That means the value of your savings actually shrinks by 3% annually.

Increases interest rates

Central banks often hike interest rates to combat inflation. While this can benefit savers through higher returns on savings accounts and bonds, it also makes borrowing more expensive. As inflation increases, so can interest rates on things like loans and mortgages.

Since inflation decreases purchasing power, lenders often hike up interest rates to account for the decreased value of the money they’ll be paid in the future.

Higher interest rates cam make it harder for individuals and businesses to access credit, slowing down economic growth.

Boosts real estate and value stocks

As inflation increases, so do property values and housing prices. That means real estate investors will see appreciation in their assets.

Additionally, value stocks—stocks that are trading below their true value—tend to fare better during periods of high inflation compared to growth stocks, or stocks that typically deliver higher returns at a faster rate.

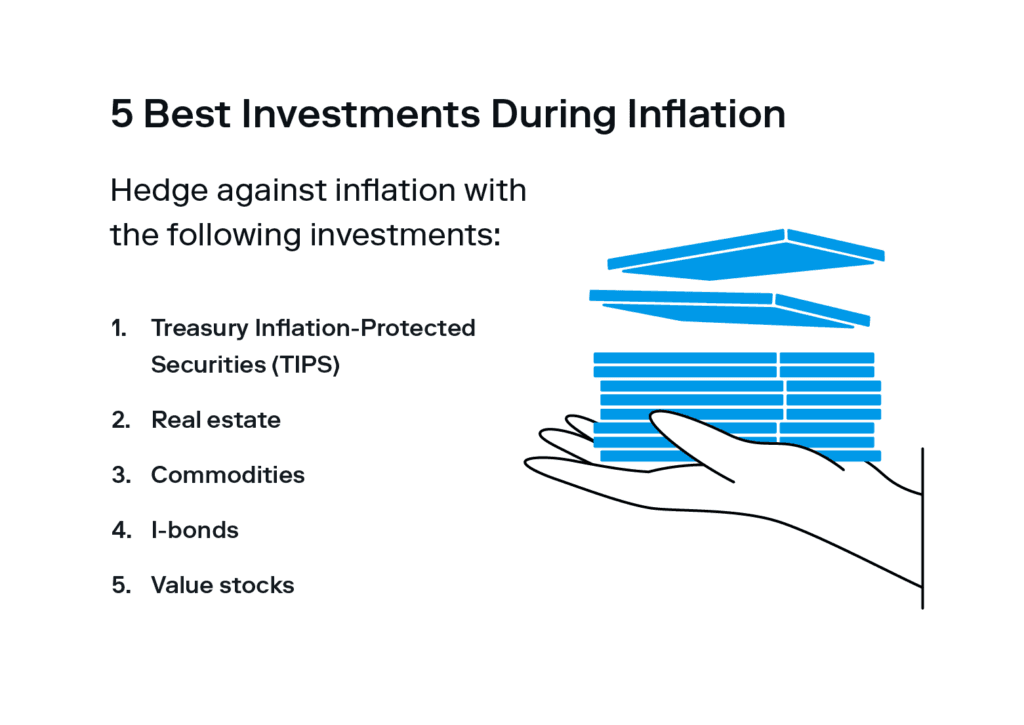

Top-performing investments during inflation

If you’re wondering how to profit from inflation, some investments perform better than others. Consider the following when deciding where to put your money.

TIPS

Treasury Inflation-Protected Securities, or TIPS, are a type of bond issued by the U.S. Treasury for the purpose of protecting investors from decreasing purchasing power.

TIPS are indexed to adjust in price as inflation rises, as measured by the Consumer Price Index (CPI). Interest payments also adjust, ensuring your investment keeps pace with rising prices.

This makes them an attractive investment option for investors looking to preserve their capital.

Real estate

Real estate investments financed with a fixed mortgage rate are traditionally a wise bet during times of inflation. As mentioned, property values increase in tandem with rising inflation—but with a fixed mortgage rate, your monthly mortgage stays the same.

You can invest in real estate by buying property directly or by buying shares of a real estate investment trust (REIT), which allows you to own shares in real estate companies. This method works well if you don’t have the cash, time, or experience to buy and manage your own property.

Commodities

Commodities include things like raw materials and natural resources—think gasoline, steel, corn, or lumber—that are necessary for the production of goods.

Prices for commodities usually rise as inflation increases, which is why they can act as an “inflation hedge”, or a way to protect against inflation. As with most investments, inflationary hedge or not, commodity prices can still be volatile. Instead of going all in on a single commodity, investors can diversify within commodities by investing in multiple types of commodities, such as metals, energy products, and agricultural goods. This allows for a more balanced portfolio that is not overly dependent on the performance of one particular commodity.

Additionally, investors can choose to invest in different forms of commodities, such as physical assets like gold or through exchange-traded funds (ETFs) or mutual funds that track commodity indexes. This can help mitigate risk by spreading investments across different types of assets and reducing exposure to market volatility.

I-bonds

Similar to TIPS, I-bonds (or inflation-indexed bonds) are designed to keep pace with inflation, making them a good investment if you’re wondering how to profit from inflation.

While you won’t see incredibly high returns from I-bonds, they do practically guarantee that you’ll earn back your principal investment—making them a good way to protect your purchasing power and add a low-risk asset to your portfolio. This becomes important during times of high inflation, when other investments like stocks are likely to plummet in value.

Value stocks

As mentioned above, value stocks tend to perform better during inflation than growth stocks. While their prices aren’t likely to increase as aggressively as growth stocks, they’re less volatile overall.

Value stocks tend to have low share prices relative to the company’s financial performance. For example, a company with a record of rising sales, earnings, and a positive cash flow represents an attractive investment, so the share price is likely to be higher. These companies can pass on cost increases to consumers, protecting their profit margins and offering investors stability. If a company checks all of those boxes but you see their share prices are relatively cheap, it’s likely a value stock.

Growth stocks, on the other hand, may struggle as higher prices may result in lower demand for their products or services.

Pros and cons of investing during inflation

Pros | Cons |

|---|---|

Preserves portfolio value | Exposure to risk |

Maintains purchasing power | Derailment of long-term goals |

Diversifies investments | Unbalanced asset allocation |

Every investment has pros and cons based on when you invest in them, and investing during inflation is no different. Here are the main advantages of investing during inflation:

It can help you preserve your portfolio’s value.

It offers an opportunity to review your portfolio and rebalance it if necessary.

This might lead you to realize that you need to further diversify your portfolio, which is always a good idea—inflation or not.

Here are the main disadvantages of investing during inflation:

You’re faced with more investment risk no matter what asset you choose.

You could risk swaying from your long-term goals by allocating more toward those investments in response to inflation.

You could risk overweighting your portfolio in a certain asset class.

The most important thing to remember is that there are no surefire answers to the question of how to profit from inflation, or how to turn a profit even when the market is strong.

Instead, it’s best to focus on what you can control—meaning knowing your ideal risk level, regularly rebalancing your portfolio, and keeping a long-term frame of mind when it comes to riding out tough economic times.

Investing made easy.

Start today with any dollar amount.

Written by

Team Stash

We want to turn money into a source of hope and opportunity. We teach people how to build good habits, save more and make it easy and affordable to get started investing. So far, we’ve helped over 6 million people create a more secure financial future with our expert advice and award winning investing app.

Related articles

investing

Jun 25, 2026

Should You Buy IPOs? 4 Myths About Hot New Listings

investing

Jun 18, 2026

Best Index Funds for Beginners and How to Pick One

investing

Jun 10, 2026

What Is an Index Fund? A Complete Beginner's Guide

investing

Jun 09, 2026

How to Start Investing: A Beginner’s Guide for 2026

investing

Jun 04, 2026

What Is Quantum Computing? An Investor’s 2026 Guide

investing

Jun 03, 2026

What Is an IPO? How It Works for Everyday Investors

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.